Buying property in Singapore is one of the most significant financial decisions you will ever make, yet many buyers assume all private property ownership is permanent. That assumption can cost you. What is freehold property exactly, and how does it differ from the leasehold arrangements that dominate Singapore’s land market? The answer shapes your resale value, financing options, and whether your property remains an asset across generations. This guide cuts through the confusion, explains what freehold ownership actually means in Singapore’s context, and helps you decide whether paying the premium makes sense for your goals.

Table of Contents

- What is freehold property in Singapore?

- Comparing freehold and leasehold: key differences and price premiums

- Understanding lease decay and its impact on property value

- Is freehold property worth the premium? Matching tenure to your holding horizon

- Common misconceptions and practical tips when buying freehold property in Singapore

- Why tenure matters more than price: a fresh perspective for Singapore buyers

- How Aesthetic Havens supports your freehold property decisions in Singapore

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Freehold ownership | Means perpetual ownership of land and building with no lease expiry in Singapore. |

| Price premium | Freehold properties usually cost 10-20% more than similar 99-year leasehold properties. |

| Lease decay | Leasehold properties lose value as the lease shortens, especially after 50 years remaining. |

| Holding horizon matters | Freehold suits long-term holds; leasehold can be better for short to medium holding periods. |

| Verify tenure | Always confirm property tenure via official records, as marketing terms can be misleading. |

What is freehold property in Singapore?

Freehold property means you own the land and the building on it indefinitely. There is no expiry date on your ownership. In legal terms, this is called an “estate in fee simple,” which is the highest form of private land title recognized under Singapore law. When you pass away, the property can be inherited by your heirs without any reverting back to the state.

This stands in sharp contrast to how most Singapore properties actually work. Freehold in Singapore is the fullest form of private land tenure, offering perpetual ownership rather than a fixed lease term. Most private condominiums, apartments, and even all HDB flats sit on 99-year leasehold land. When the lease ends, ownership reverts to the Singapore government, specifically to the state through the Singapore Land Authority.

Freehold properties are relatively rare in Singapore for a specific historical reason. Most of them originated from land grants issued during the colonial era, largely before 1960. Because the Singapore government retains most of the island’s land and issues primarily leasehold titles, freehold stock makes up a small fraction of total residential property here.

Key distinctions that define freehold ownership in Singapore:

- Perpetual title: No countdown clock on your ownership

- Inheritance rights: You can pass the property to heirs without lease limitations

- No reversion risk: The state cannot reclaim the land when a lease ends because there is no lease

- Greater financing stability: Banks and CPF Board treat freehold properties more favorably as the asset ages

Understanding freehold property explained at this foundational level is critical before you evaluate any listing, whether you are buying your first home or expanding an investment portfolio.

Comparing freehold and leasehold: key differences and price premiums

Once you understand what freehold means, the next question is practical: what does it actually cost you, and what do you get in return?

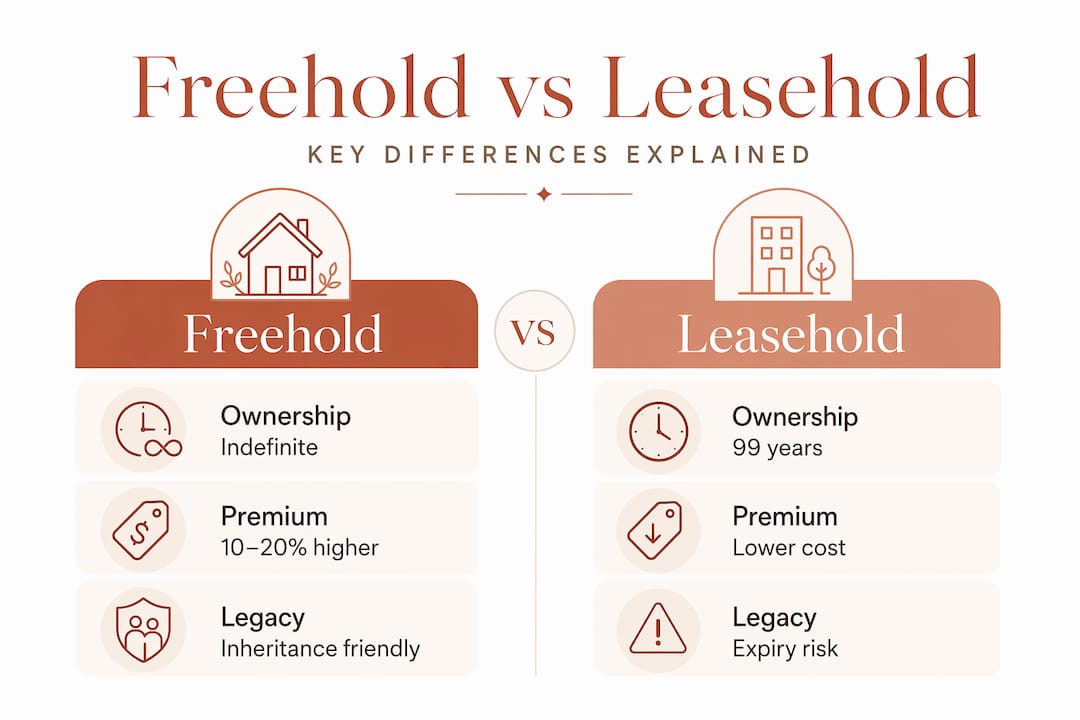

The most direct answer is that freehold stock commands a 10–20% premium over comparable 99-year leasehold properties in Singapore. That gap varies depending on location, remaining lease on competing leasehold units, and overall market conditions. In prime districts like District 9 or 10, the premium can push toward the upper end of that range because freehold supply is especially constrained.

| Feature | Freehold | 99-Year Leasehold |

|---|---|---|

| Ownership duration | Indefinite | Fixed, typically 99 years |

| Entry price | Higher (10–20% premium) | Lower |

| Lease decay risk | None | Significant after 50+ years |

| CPF usage | Unrestricted | Restricted as lease shortens |

| Financing (LTV) | Full LTV regardless of age | Reduced for older leasehold units |

| Inheritance | Unrestricted | Limited by remaining lease |

| En bloc potential | Strong | Moderate |

Leasehold properties lose value as the remaining lease shortens, a process called lease decay (covered in detail in the next section). This property depreciation effect is not hypothetical. It is a measurable, documented risk that changes how buyers, banks, and CPF treat your asset over time.

Why freehold property matters to long-term investors:

- Exit value protection: A freehold unit retains its title regardless of when you sell

- Wider buyer pool: More buyers qualify for financing on freehold units regardless of the unit’s age

- Stronger en bloc prospects: Freehold sites are more attractive for redevelopment bids because developers do not need to factor in lease top-up costs

- Generational wealth transfer: You can include it in estate planning without lease expiry complicating valuations

For context on why Singapore property remains a cornerstone of wealth building in Asia, tenure is one of several factors that make certain assets more defensible than others.

Pro Tip: If you are comparing two units in the same condo development where one is freehold and the other leasehold due to a boundary difference, always check the actual land title. Developments on the boundary between freehold and leasehold land do exist, and the marketing materials do not always make this obvious.

Understanding lease decay and its impact on property value

Lease decay is the single most underestimated risk in Singapore property investment. Most buyers focus on current value and rental yield. Far fewer map out what their property will be worth when the lease drops below 60 years.

The depreciation of leasehold properties accelerates sharply in the final decades of the lease, dropping from roughly 60% of original value at 30 years remaining to about 17% at 5 years remaining. That is not a gradual decline. It is a cliff.

Here is how lease decay plays out in practice across a typical property’s lifespan:

- Years 1 to 40: Value broadly tracks market movements. Lease decay has minimal visible impact. Buyers are willing and financing is unrestricted.

- Years 41 to 60: Subtle shifts begin. Some buyers start requesting discounts. CPF usage starts becoming subject to conditions.

- Years 61 to 75: Financing tightens. Banks apply stricter LTV ratios. CPF Board may limit how much you can use for purchase or refinancing.

- Years 76 to 85: The buyer pool shrinks considerably. Only cash-heavy buyers or investors with specific redevelopment intent remain active. Prices begin dropping more visibly.

- Years 86 to 99: Value collapses. The asset becomes largely illiquid except at steep discounts. Most CPF usage is disallowed.

“Freehold properties avoid this depreciation curve entirely. They maintain a value floor tied to land scarcity and location rather than an expiring clock.”

For buyers thinking about property inheritance and legacy planning, freehold ownership removes an entire layer of risk from the equation. Your heirs will not inherit a ticking time bomb.

An investment property depreciation schedule for a leasehold property looks very different from a freehold one. For freehold, the structural depreciation of the building matters, but the land component retains its value indefinitely. For leasehold, both the building and the land entitlement lose value simultaneously as the clock winds down.

Is freehold property worth the premium? Matching tenure to your holding horizon

This is the right question, and most buyers never ask it precisely enough. The answer depends almost entirely on how long you plan to hold the property.

Freehold is structurally better for long holding periods of 30 years or more and for legacy planning, while leasehold can be more competitive for shorter holds under roughly 15 years. That framework alone should guide most purchase decisions.

Here is how to apply it to your situation:

- If you are buying a forever home for your family and plan to pass it down: freehold’s perpetual title is worth the premium. The extra 10–20% upfront is small compared to the compounding value of an asset your children can inherit without constraints.

- If you are buying to rent and sell within 10 years: A newer leasehold unit at a lower entry price often produces better risk-adjusted returns. Lease decay will not bite within that window, and you will have deployed less capital.

- If you are buying for your retirement years: Consider your age plus the likely holding period. If the remaining lease falls below 30 years before you turn 80, financing and CPF complications become personal, not just theoretical.

- If you are building a multi-property portfolio: Mix freehold and leasehold strategically. Use lower-entry leasehold for yield plays and freehold for capital preservation anchors.

The opportunity cost argument is real. The freehold premium paid today could be invested elsewhere for potentially strong medium-term gains. But that math changes when you account for the progressive illiquidity of aging leasehold stock and the compression in buyer pool it causes.

Freehold also provides practical financing advantages. CPF access is unrestricted. Banks apply standard LTV ratios regardless of how old the property is. That matters both when you buy and when your future buyer needs financing to purchase from you.

For a broader view on buying property in Singapore, including how tenure interacts with stamp duties and financing structures, matching tenure to your personal holding strategy is a core part of any sound purchase decision.

Pro Tip: Don’t over-index on the label “freehold equivalent” when evaluating listings. Some 999-year leaseholds carry this description in marketing materials. While a 999-year lease is far better than 99 years, it is not legally identical to freehold. Know the exact tenure before you commit.

Common misconceptions and practical tips when buying freehold property in Singapore

The Singapore property market is well-informed but not immune to marketing-driven confusion. A few persistent myths affect how buyers evaluate freehold versus leasehold options.

Misconception 1: “Freehold equivalent” means freehold. It does not. Verify tenure through official land title records because “freehold equivalent” sometimes refers to 999-year leaseholds, which are legally distinct from true freehold ownership. Check the land title documents directly through Singapore Land Authority records or your solicitor before signing anything.

Misconception 2: All private property is freehold. Many buyers are surprised to learn that private condominiums, landed homes, and shophouses can all be leasehold. Private ownership does not equal perpetual ownership.

Misconception 3: Leasehold properties near MRT stations always outperform freehold. Location does matter enormously, but a leasehold unit with 40 years remaining near an MRT will still face the financing and liquidity wall described earlier. Location delays lease decay but does not eliminate it.

Practical tips for verifying tenure before you buy:

- Request the title document from the seller’s solicitor and confirm the tenure classification

- Check the SLA’s Integrated Land Information Service for land tenure details

- Confirm whether the land lot is classified as freehold, 999-year, 99-year, or another tenure variant

- Ask specifically about en bloc history or any government acquisition notices if you are buying older freehold units

- For older freehold properties, confirm no outstanding charge or encumbrance that would affect clean title transfer

Pro Tip: Scrutinize any listing that uses the word “perpetual” without specifying freehold. Agents sometimes use perpetual loosely. The only perpetual ownership in Singapore’s property market is true freehold. Ask for the land title document, not the marketing brochure.

Why tenure matters more than price: a fresh perspective for Singapore buyers

Here is the view that most property articles never give you: freehold ownership is not a luxury add-on to a property purchase. It is a risk management tool. Treating it as just a label on a listing, or as a premium you either accept or reject, misses the deeper function it serves.

Treating freehold vs leasehold as just a label ignores how tenure shapes long-run exit value and how the market and financiers perceive resale risk. The premium you pay on day one is visible. The discount you may face at resale due to lease decay is invisible until it arrives.

There is also a behavioral finance dimension here that most buyers overlook. When you hold a leasehold property and watch the lease drop below 70 years, you become a motivated seller whether you want to be or not. You lose negotiating power. Your buyer pool shrinks. Your bank tightens. Freehold ownership preserves your optionality. You sell when you choose to, not when the lease forces your hand.

Many buyers overvalue perpetual ownership in short holds and undervalue it in very long ones. The investor who buys a leasehold unit, collects strong rental yield for 12 years, and exits cleanly before lease decay kicks in has made a rational decision. But the buyer who plans to live in a property for 30 years and chooses leasehold to save 15% upfront may find that decision reverses in the final decade of their hold.

For buyers thinking about property inheritance and legacy planning, freehold tenure is not just about resale value. It is about what kind of asset you are passing down. A property with 40 years of lease remaining is not a gift to your children. It is a liability.

Price is easy to calculate. Tenure’s long-run impact requires a longer view. Build that view before you sign.

How Aesthetic Havens supports your freehold property decisions in Singapore

Understanding freehold property explained in theory is one thing. Applying it to an actual purchase decision in today’s Singapore market is another.

At Aesthetic Havens, our real estate advisory services are built specifically for buyers and investors who want to make tenure-informed decisions, not just chase the lowest price or the newest launch. Our team helps you:

- Verify land tenure through title documents and official records before any commitment

- Assess the freehold premium relative to your holding period and exit strategy

- Match property to your investment timeline, whether that is a 5-year rental play or a generational asset

- Navigate CPF and financing rules specific to freehold and leasehold properties

- Negotiate with market intelligence backed by current sales data and comparable analysis

Whether you are a first-time buyer or expanding a portfolio, our agents across Singapore bring the depth of knowledge that makes the difference between a good deal and the right one. If you are ready to explore Singapore property as an investment, we are ready to guide you through every step with clarity and confidence.

Frequently asked questions

What does freehold property mean in Singapore?

Freehold property in Singapore means you own both the land and building indefinitely with no expiry date. As the fullest form of private land tenure, it gives you perpetual ownership rights rather than a fixed lease term like the more common 99-year leasehold.

Is freehold property always better than leasehold?

Not always. Freehold suits very long holding periods of 30 or more years and legacy planning, while leasehold can offer better risk-adjusted returns for shorter holds under 15 years due to its lower entry price.

How much more does freehold property cost compared to leasehold?

Freehold properties typically command a 10–20% premium over comparable 99-year leasehold properties, with variation depending on location, property age, and remaining lease on competing leasehold stock.

Can I rely on marketing terms like “freehold equivalent” when buying?

No. “Freehold equivalent” sometimes refers to 999-year leaseholds, which are legally distinct from true freehold. Always verify tenure through official land title records before making a purchase commitment.

How does freehold affect financing in Singapore?

Freehold properties carry no lease-related CPF or LTV restrictions, meaning you can access full CPF usage and standard loan-to-value ratios regardless of the property’s age or your holding timeline, which makes financing considerably more flexible.