Buying commercial property in Singapore is one of the most significant financial decisions a business owner can make. The opportunity is real: no Additional Buyer’s Stamp Duty (ABSD), higher rental yields compared to residential, and strong long-term demand. But the process is layered with zoning regulations, financing rules, legal requirements, and due diligence steps that catch unprepared buyers off guard. One wrong move, such as missing a URA restriction or skipping a title check, can cost you hundreds of thousands of dollars. This guide breaks down every critical step, from understanding property types to completing ownership transfer, so you can move forward with clarity and confidence.

Table of Contents

- Understanding commercial property types & market conditions

- Preparing to buy: Budget, loans, and legal requirements

- Step-by-step process: From search to completion

- Key risks, pitfalls, and what to verify before and after purchase

- Our perspective: What most buyers miss about Singapore commercial property

- How Aesthetic Havens can help your commercial property journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your property type | Identify the right type of commercial property—retail, office, industrial, or hotel—based on your business or investment goals. |

| Prepare your finances | Arrange 20% cash downpayment, gather corporate documents, and understand loan limits before starting your search. |

| Master the process | Follow a clear step-by-step procedure from research to completion and pay careful attention to legal and regulatory details. |

| Diligence beats hype | Strong returns are possible, but rigorous due diligence and checking compliance are your best protection against costly mistakes. |

Understanding commercial property types & market conditions

Before you start browsing listings, you need to know what you’re actually buying and whether it fits your goals. Types of commercial property in Singapore fall into four main categories: retail (shophouses, malls), office (Grade A, B, and C), industrial (B1 and B2), and hotels. Each is zoned by the URA Master Plan with specific usage rules that cannot be ignored. A B1 industrial unit, for example, allows clean, light manufacturing. A B2 unit permits heavier industrial use. An office zoned building cannot be legally used as a warehouse.

Here’s a quick comparison to help you match property type to purpose:

| Property type | Typical use | Zoning category | ABSD applicable? |

|---|---|---|---|

| Retail shophouse | F&B, retail, services | Commercial | No |

| Grade A office | Corporate HQ, MNC | Commercial | No |

| B1 industrial | Light manufacturing, logistics | Industrial | No |

| B2 industrial | Heavy industrial, storage | Industrial | No |

| Hotel | Hospitality, short-term stays | Hotel | No |

The market data for 2026 is worth paying attention to. Commercial property transactions in Singapore hit S$17 billion in 2025, with industrial prices rising 1.4% quarter on quarter and office rents holding firm. This signals a market that rewards buyers who act on solid fundamentals, not speculation.

What makes commercial property appealing compared to residential?

- No ABSD, which means significant savings especially for investors already holding residential assets

- Higher rental yields, typically 4% to 6% versus 2% to 3% for residential

- Longer lease tenancies, which stabilize cash flow

- Business operational flexibility, particularly useful for owner-occupiers

Before finalizing any property, check Singapore property trends 2026 to understand sector-by-sector dynamics. Always verify zoning and permitted uses on URA SPACE before committing to any offer. This one check alone can save you from an expensive compliance headache.

Preparing to buy: Budget, loans, and legal requirements

With the market and property types in mind, the next step is to get your finances and legal paperwork in order. Commercial property financing works differently from residential, and many buyers are surprised by how strict the requirements are.

Here’s what you need to know about financing:

| Financing factor | Requirement |

|—|—|— |

| Maximum LTV | Up to 80% (bank loan) |

| Minimum cash downpayment | 20% |

| Loan tenure | Up to 25 to 30 years |

| TDSR cap | 60% of gross monthly income |

| CPF usage | Not permitted |

For bank loan information, corporate buyers face additional criteria: your company must have at least 30% local ownership and typically one to two years of incorporation history. Lenders want to see that your business is established and financially stable before extending credit.

Documents you need to prepare:

- ACRA business profile (not older than three months)

- Audited financial statements for the past two years

- Latest six months of company bank statements

- Directors’ NRIC or passport copies

- Any existing tenancy agreements if the property generates rental income

For Singapore mortgage requirements, individual buyers face TDSR calculations that include all existing debt obligations. If your personal borrowings are already high, this can limit how much you can borrow for a commercial purchase. Plan ahead.

Pro Tip: Get an in-principle approval (IPA) from your preferred bank before you make any offer. An IPA signals to sellers that you’re serious and financially ready, which can strengthen your negotiating position.

Foreign buyers should check foreigner eligibility rules carefully. Most commercial property types are open to foreigners, but specific restrictions may apply depending on the property category and structure of ownership.

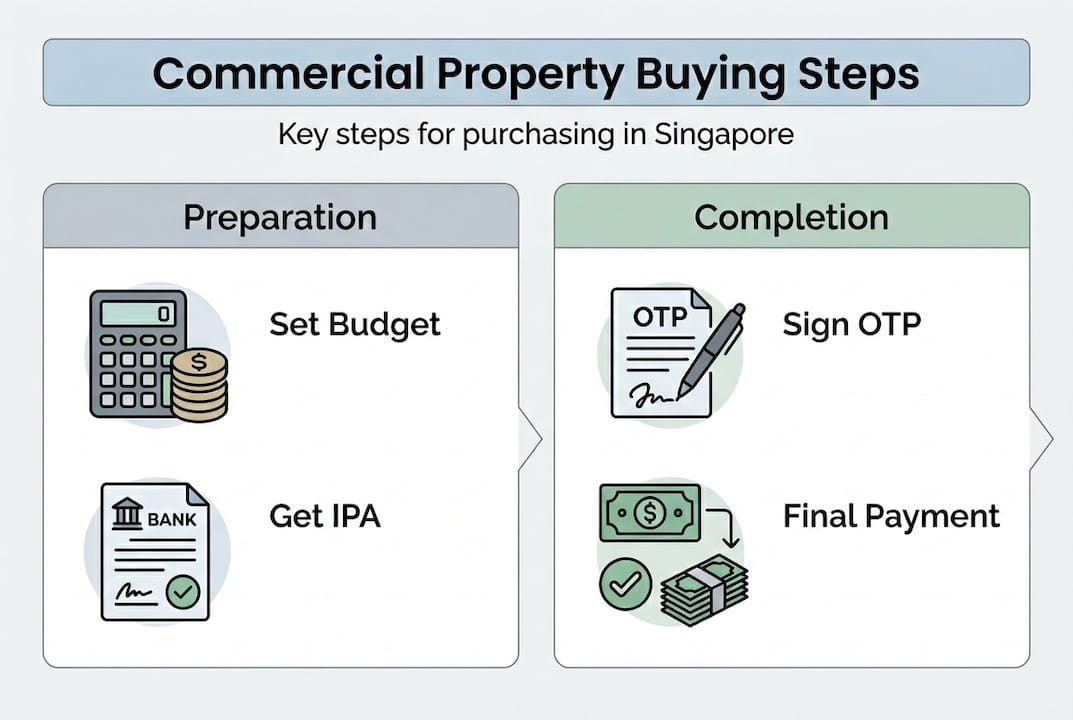

Step-by-step process: From search to completion

Once you’re prepared with your budget and paperwork, here’s exactly how to navigate the process from first search to final ownership transfer.

- Research and shortlist. Use PropertyGuru, EdgeProp, or the URA zoning compliance portal to find properties that match your usage and budget. Filter by zone, tenure (freehold vs. leasehold), and sector.

- Engage a licensed agent and lawyer. Your agent handles negotiations, market comparisons, and paperwork coordination. Your lawyer conducts title searches, reviews the Option to Purchase (OTP), and manages the legal transfer.

- Conduct initial due diligence. Verify zoning, existing tenancies, outstanding maintenance fees, and any caveats registered against the property.

- Negotiate and secure the OTP. Pay a 1% option fee to secure the OTP, which is typically valid for 14 to 21 days. Use this window to complete financing and legal checks.

- Apply for financing. Submit your loan application with all documents ready. Approval can take one to two weeks.

- Sign the Sale and Purchase Agreement (SPA). Once financing is approved, your lawyer prepares and executes the SPA.

- Pay stamp duties and GST. Buyer’s Stamp Duty (BSD) applies. If the seller is GST-registered and the property is not residential, 9% GST applies to the purchase price.

- Complete and transfer title. Completion of the process typically takes 8 to 12 weeks from the OTP date.

For a deeper walkthrough, read the complete buying process guide which covers every legal and financial milestone in detail.

“Rushing the OTP stage without completing your due diligence is the single most common and most costly mistake buyers make. The 14-day window exists for a reason. Use it fully.”

Pro Tip: Ask your lawyer to check for any outstanding charges, URA compliance notices, or tenancy disputes before signing the SPA. These issues do not disappear after completion; they transfer to you as the new owner.

Key risks, pitfalls, and what to verify before and after purchase

After mapping out the full buying journey, it’s essential to protect yourself by proactively identifying risks and verifying every requirement.

The commercial market carries compelling upside, but as expert risk perspectives note, more attractive LTV ratios versus residential come paired with higher risks and costs that demand a robust focus on fundamentals, given the resilient yet cyclical 2026 outlook.

Top risks to watch:

- Zoning violations. If a tenant is operating outside the permitted URA use, you inherit that liability at completion.

- Title defects. Unresolved caveats, outstanding mortgages, or disputed ownership can delay or derail the transaction.

- Tenancy traps. A sitting tenant with an unfavorable lease can lock you into below-market rents for years.

- Market cycle exposure. Office and retail rents can shift significantly within a one to two year window.

- Stamp duty miscalculations. GST and BSD must be computed correctly to avoid penalties.

Due diligence checklist before signing:

- Confirm URA zoning and permitted uses on URA SPACE

- Run a title search through your lawyer

- Review all tenancy agreements for break clauses and expiry dates

- Check for any outstanding MCST or management fees

- Confirm that the seller is GST-registered if applicable

Post-purchase steps are often overlooked. After completion, you need to register the transfer with the Singapore Land Authority (SLA), update ACRA records if purchasing under a corporate entity, and formally take over property management from the previous owner.

Explore the commercial investment benefits alongside the risks to build a balanced view before committing.

“Verification is not paperwork. It is protection. Every box you skip becomes a potential liability that surfaces months after you’ve signed.”

Pro Tip: Commission an independent property valuation before making an offer. This gives you a benchmark for negotiation and confirms that you’re not overpaying in a market where listed prices can reflect seller optimism more than actual market value.

Our perspective: What most buyers miss about Singapore commercial property

Here is our honest take after working with buyers across multiple commercial sectors in Singapore. The no-ABSD advantage and 80% LTV ceiling draw many business owners in, and rightly so. But what often goes unexamined is the full cost of holding a commercial asset: maintenance fees, property tax (which is higher than residential), insurance, vacancy periods between tenancies, and potential renovation costs to suit new tenants.

The buyers who succeed long-term are not chasing yield percentages. They are buying into locations with genuine tenant demand, clear zoning that supports their business model, and properties with manageable holding costs relative to expected cash flow.

Timing also matters more than most people admit. The 2026 commercial property trends show a resilient market, but cycles do turn. Buying at the right price, in the right zone, with the right tenant profile is still the formula that outperforms every shortcut.

How Aesthetic Havens can help your commercial property journey

For entrepreneurs who want peace of mind and expert support, here’s how professional help makes all the difference.

Navigating Singapore’s commercial property market without guidance is like trying to pass a compliance audit without an accountant. The rules are specific, the stakes are high, and the details matter enormously. At Aesthetic Havens, we coordinate the full process: property selection, negotiation strategy, URA compliance checks, financing coordination, and legal handover. Understanding the real estate agents’ benefits becomes clear when you see how much time, risk, and money professional guidance saves. Whether you’re buying your first commercial asset or expanding your portfolio, the investing benefits are maximized when every step is handled by someone who knows the terrain.

Reach out to us for a no-obligation consultation and let’s map out a strategy that fits your business and investment goals.

Frequently asked questions

What types of commercial property can I buy in Singapore?

You can buy retail, office, industrial (B1/B2), and hotel properties, each with zoning and usage restrictions set by the URA Master Plan.

How much downpayment do I need to buy commercial property?

You need a minimum 20% cash downpayment since CPF funds cannot be used for commercial property purchases in Singapore.

How long does the buying process for commercial property take?

From offer to completion takes 8-12 weeks after securing an OTP, though complex legal checks or financing delays can extend this timeline.

Can foreigners buy commercial property in Singapore?

Yes, foreigners can purchase most types of commercial property in Singapore, subject to specific restrictions and regulatory checks depending on the property category.

What is the URA, and why does its zoning matter?

The URA (Urban Redevelopment Authority) assigns each property a specific zoning classification that legally determines which business activities are permitted on the premises.

Recommended

- How to Buy Commercial Property in Singapore: A Step-by-Step Guide | Aesthetic Havens

- Foreigner’s Guide to Buying Property in Singapore (2025 Regulations & Taxes) | Aesthetic Havens

- Top benefits of investing in commercial property in Singapore

- Essential landlord roles in leasing: A Singapore guide

- Commercial relocation explained: move offices efficiently