Selling property in Singapore feels straightforward until you’re actually in it. Most sellers assume there’s one universal checklist to follow, but the reality is that Singapore operates two legally distinct sales processes: one for HDB resale flats and another for private residential property. Each track carries its own forms, regulatory authorities, timelines, and legal requirements. Whether you’re selling your first HDB flat or a private condominium, understanding which track governs your transaction and exactly what each step requires is what separates a smooth completion from a costly, stressful delay.

Table of Contents

- Understanding Singapore’s property sales process: Two main tracks

- Step-by-step breakdown: HDB resale flat sales process

- Step-by-step breakdown: Private property sales process

- HDB vs. private: Key differences every seller and buyer should know

- What most guides miss about the Singapore property sales process

- How expert guidance streamlines your Singapore property transaction

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Two main sales tracks | Singapore property transactions follow distinct HDB and private property sales processes. |

| HDB steps are regulated | The HDB resale process requires specific portal actions, government approval, and defined milestones. |

| Private sales need lawyers | Private property sales depend on lawyer-led documentation and contract compliance, including caveat lodging. |

| Timelines vary by type | Expect longer, government-driven timelines for HDB and contract-driven schedules for private deals. |

| Expert guidance reduces risk | Engaging knowledgeable agents or advisors minimizes costly documentation errors and regulatory delays. |

Understanding Singapore’s property sales process: Two main tracks

Singapore’s property market is built on a fundamental divide between public housing, governed by the Housing and Development Board (HDB), and private residential property, regulated under frameworks set by the Urban Redevelopment Authority (URA) and the Council for Estate Agencies (CEA). This isn’t just administrative tidiness. The dual-track system reflects deeply different policy goals, buyer eligibility rules, and price control mechanisms.

Think of the property sales process as two parallel tracks: (1) contract and option formation, and (2) regulatory and administrative milestones, as the CEA’s own guidance on selling an HDB flat explains. These two dimensions run simultaneously, and losing track of either one creates real problems.

For HDB resale transactions, the government sits firmly in the driver’s seat. HDB’s own “Overview of Flat Selling Process” is the authoritative high-level starting point for the resale-selling flow and next steps. Every stage, from listing to completion, must pass through the HDB Resale Portal, and buyers face strict eligibility requirements before any sale can proceed.

Private property sales, on the other hand, are market-driven. The URA provides standard contract templates, and the CEA sets professional conduct standards for agents. But the responsibility for legal compliance, document preparation, and risk management rests on the parties and their lawyers rather than a government portal.

Key structural differences at a glance:

| Feature | HDB resale | Private property |

|---|---|---|

| Governing authority | HDB | URA / CEA |

| Portal required | Yes (HDB Resale Portal) | No central portal |

| Buyer eligibility check | Mandatory before OTP | Not required |

| Lawyer involvement | Optional (recommended) | Mandatory |

| Standard OTP template | Yes (HDB prescribed) | Yes (URA prescribed) |

| Caveat lodging | Not required | Compulsory for buyers |

First-timers are often blindsided by three things in particular: the strict OTP document templates (you cannot simply draft your own), HDB’s eligibility and prior approval requirements that can delay or block a sale, and the mandatory lawyer involvement in private transactions. If you’re also exploring buying commercial property, the legal structure is different again, adding another layer of complexity worth understanding early.

Pro Tip: Before listing your property, whether HDB or private, consult an experienced agent who can map your specific situation against the right regulatory track. The wrong assumption here sets off a chain reaction of problems.

Good home staging can also make a significant difference in how quickly your property sells, giving you better leverage regardless of which track you’re on.

Step-by-step breakdown: HDB resale flat sales process

Now that you understand why the process isn’t one-size-fits-all, let’s clarify how each track works in detail, starting with HDB resale.

In Singapore, selling a resale HDB flat generally starts with registering an Intent to Sell on the HDB Resale Portal, a step many sellers overlook or underestimate in its importance. This registration triggers a Minimum Occupation Period (MOP) check and informs potential buyers of the flat’s eligibility for purchase. Without completing this step, you cannot legally proceed with any transaction.

Here’s the full sequence for selling your HDB flat:

- Register Intent to Sell on the HDB Resale Portal. You’ll receive a confirmation of your eligibility to sell.

- Market your flat and begin negotiations with potential buyers. You can engage an agent at this stage.

- Grant the Option to Purchase (OTP) to the buyer using HDB’s prescribed template. You receive a 1% option fee, and the buyer has 21 days to decide.

- Buyer exercises the OTP by paying the remaining option fee (up to 4%) within the stipulated window.

- Both parties submit their respective portions of the resale application on the HDB portal, typically within 7 days of OTP exercise.

- Endorse documents and pay required fees digitally through the HDB portal.

- Await HDB’s resale approval, which includes checks on buyer eligibility, grant entitlement, and financial compliance.

- Attend the completion appointment at HDB Hub, where ownership is formally transferred.

After the buyer exercises the HDB OTP, the seller and buyer submit their respective portions of the resale application, then endorse documents and pay fees, before HDB grants resale approval and the completion appointment is attended, as outlined by the CEA.

Timeline snapshot:

| Stage | Estimated timeframe |

|---|---|

| Intent to Sell to OTP grant | 1 to 4 weeks |

| OTP exercise period | Up to 21 days |

| Resale application submission | Within 7 days of OTP exercise |

| HDB processing and approval | 4 to 8 weeks |

| Completion appointment | Scheduled after approval |

According to HDB resale timeline data, the period after OTP exercise typically covers HDB application processing followed by the completion appointment, with total transaction time averaging 8 to 12 weeks from OTP exercise. Many sellers budget for 6 weeks and are then scrambling when HDB takes longer during peak periods.

Pro Tip: Submit your resale application within the first 3 days after OTP exercise, not at the 7-day deadline. Earlier submission reduces the risk of errors bouncing back and eating into your processing window.

Staying informed on recent HDB resale market trends will also help you price and time your sale accurately. And when it comes to selecting representation, choosing the right HDB agent with proven resale transaction experience is one of the most important decisions you’ll make.

Step-by-step breakdown: Private property sales process

Having covered the structured HDB route, let’s walk through the private property track and see where legal and market forces change your obligations as a seller.

Private residential property transactions in Singapore, covering condominiums, apartments, landed homes, and executive condominiums after the MOP, are guided by URA and CEA resources including standard contract templates like the prescribed Option to Purchase and the Sale and Purchase Agreement (S&P). Unlike HDB, there is no single government portal governing the transaction, which means coordination between your agent, your lawyer, and the buyer’s side requires much tighter management.

Here is the step-by-step sequence for a private property sale:

- Negotiate price and terms with a potential buyer, typically through agents on both sides.

- Issue the Option to Purchase (OTP) using the URA-prescribed form. The buyer pays an option fee (typically 1%) and has 14 days to exercise the OTP.

- Buyer exercises the OTP by signing and returning it with the exercise fee (typically 4-9% of purchase price, minus the option fee). This commits both parties.

- Both parties engage their respective lawyers to prepare and review the Sale and Purchase Agreement.

- S&P Agreement is signed, usually within 8 weeks of OTP exercise.

- Buyer’s lawyer lodges a caveat on the property through the Singapore Land Authority (SLA) to protect the buyer’s interest.

- Legal checks, Central Provident Fund (CPF) usage approvals, and loan drawdown are coordinated by the lawyers.

- Completion occurs on the agreed date, usually 8 to 12 weeks after OTP exercise, with keys and balance payment exchanged.

One key mechanism that surprises first-timers is the caveat. Lodging a caveat is a critical control mechanism for buyers in Singapore, functioning as a public legal notice that prevents the seller from transferring ownership to anyone else while the transaction is in progress. If a buyer’s lawyer fails to lodge the caveat promptly after OTP exercise, the buyer is exposed to risk.

Key distinctions for private property sellers:

- Lawyers are not optional. They are central to the transaction’s legal compliance.

- The caveat system creates a formal, publicly visible claim on the property.

- Timelines are contractually set, not government-dictated, so both parties need to honor agreed completion dates.

- Sellers may face Additional Buyer’s Stamp Duty (ABSD) remission deadlines if they’re upgrading.

If you’re working with buyers from outside Singapore, understanding foreigner property buying guidelines is essential, as additional restrictions and tax implications apply. Sellers should also understand their landlord legal roles if the property is tenanted at the time of sale, since existing leases create additional obligations.

Pro Tip: Ensure your lawyer and the buyer’s lawyer have agreed on a clear completion date before OTP exercise. Misaligned legal calendars have caused otherwise smooth sales to miss their deadlines and trigger financial penalties.

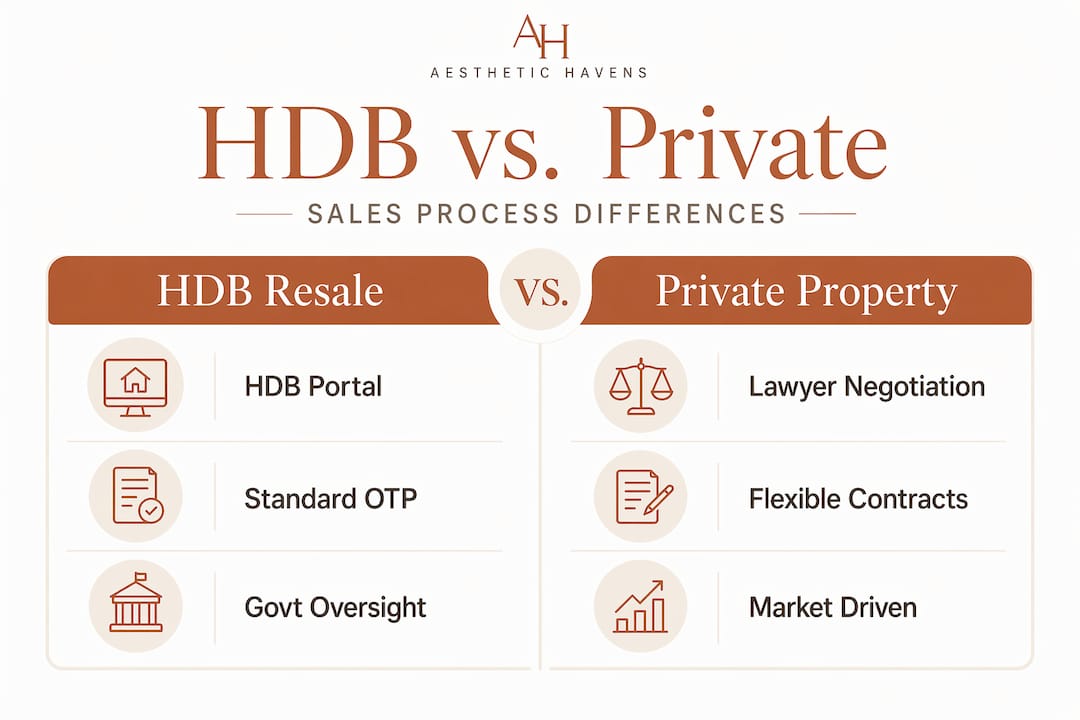

HDB vs. private: Key differences every seller and buyer should know

Now let’s lay both sales processes side by side so you can navigate with absolute clarity, no matter which property type you hold.

| Dimension | HDB resale | Private property |

|---|---|---|

| OTP template | HDB-prescribed (mandatory) | URA-prescribed (mandatory) |

| OTP exercise period | 21 days | 14 days |

| Portal submissions | HDB Resale Portal (required) | None (lawyer-led) |

| Caveat lodging | Not required | Compulsory for buyer protection |

| Timeline driver | Government processing | Contract and legal coordination |

| Buyer eligibility | Checked by HDB | No restrictions (except foreigner rules) |

| Lawyer | Recommended but optional | Mandatory for both parties |

| Government grants | CPF Housing Grants available | Not applicable |

The regulatory bodies overseeing these processes, including HDB, CEA, URA, and the Controller of Housing framework, each serve a distinct function. As the CEA’s guidance on buying or selling private residential property notes, knowing which regulator governs your transaction determines what forms, timelines, and legal obligations apply to you.

“The most expensive mistakes in Singapore property sales don’t happen at the negotiating table. They happen during document submission and regulatory timeline management, where inexperienced parties assume one process mirrors the other.”

Why these distinctions matter in practice:

- Risk control is government-managed for HDB, but buyer-initiated through caveat lodging for private transactions. Miss the caveat and you lose your protection.

- Timeline pressure is different: HDB sellers must work within HDB’s processing cycles, while private sellers face contractual deadlines that can trigger legal liability if missed.

- Documentation errors in HDB transactions bounce back from the portal with formal rejection notices. In private transactions, they may not surface until the completion itself, which is far more disruptive.

Understanding Singapore HDB resale price trends for 2025 and beyond also helps sellers time their listing correctly within each market cycle. For a historical comparison of HDB and private residential market dynamics, context matters when advising on timing and pricing strategy.

What most guides miss about the Singapore property sales process

After reviewing the two-track system, here’s some field-tested wisdom you won’t find on checklist websites.

Most sellers underestimate how much government or law firm processing timelines, not their own decisions, control the pace of their transaction. You can do everything right on your end, submit every document on time, coordinate with your buyer perfectly, and still find yourself waiting an extra 3 to 4 weeks because HDB’s resale unit is processing a high volume of applications. Or a law firm is managing simultaneous completions. These aren’t exceptional cases. They’re routine.

The second blind spot is documentation coordination. A private property transaction involves at least four parties coordinating legal documents simultaneously: your lawyer, the buyer’s lawyer, the bank’s legal panel, and CPF Board (if CPF is being used). A single missing document from any one of them can push your completion date back. Sellers who build in buffer time and assign a clear point of contact for document chasing consistently close faster.

Here’s the most common critical mistake we see: sellers who’ve sold an HDB flat before assume the private property process follows the same ordering of steps. It doesn’t. The OTP exercise window is shorter (14 vs. 21 days), the caveat lodging step doesn’t exist in HDB at all, and the entire legal workflow is reversed in priority. Treating one checklist as interchangeable with the other creates gaps that cost money to fix.

Not all agents have mastered both tracks either. An agent who specializes purely in HDB resale may not be familiar with the nuances of private property caveat lodging, ABSD remission timelines for upgraders, or coordinating with law firms handling simultaneous transactions. Understanding HDB resale market nuances is a skill, but so is the private market equivalent, and the two don’t automatically transfer.

Our practical recommendation: build your transaction timeline backward from your target completion date, identify every regulatory bottleneck (HDB processing time, SLA caveat lodging, CPF withdrawal approval), and assign a buffer to each one. Most sellers plan around the buyer-seller agreement date. The smart ones plan around the regulatory constraints that neither party can control.

How expert guidance streamlines your Singapore property transaction

Knowing the process is one thing. Executing it without gaps, missed deadlines, or costly errors is another.

At Aesthetic Havens, we guide sellers and buyers through both HDB resale and private property transactions with the kind of regulatory fluency that prevents the common pitfalls outlined in this article. Whether you’re navigating your first HDB resale or coordinating a multi-party private property completion, the right advisory support makes a measurable difference in outcome and timeline. Explore our real estate advisory guide to understand how structured expert guidance works in practice. Learn more about what a professional agent brings to your transaction, then connect with the Aesthetic Havens team to discuss your specific property goals.

Frequently asked questions

How long does it typically take to complete an HDB resale transaction?

It usually takes 8 to 12 weeks from OTP exercise to completion, subject to HDB approval timelines and application processing volumes during peak periods.

What is a caveat in Singapore property sales?

A caveat is a legal notice lodged by the buyer after securing the OTP or signing the Sale and Purchase Agreement to protect their interest in the property and prevent the seller from transferring ownership to another party.

Who prepares legal documents for private property sales?

In private transactions, both the seller and buyer engage their own lawyers to prepare and review legal documents, as required by standard contract templates prescribed by the URA.

Is the sales process different for foreigners buying property in Singapore?

Yes, foreigners face additional regulations and significantly higher stamp duties, especially for HDB and landed homes, as detailed in the foreigner property buying guide covering 2025 regulations and taxes.

What are the most common pitfalls during the sales process?

Missing documentation deadlines, using the wrong OTP template for your property type, and failing to lodge a caveat promptly after OTP exercise are the three most frequent and preventable mistakes in Singapore property transactions.