Real Estate Investment Trusts (REITs) are companies that own, operate, or finance income-producing real estate, giving investors access to diversified property portfolios without direct ownership or management responsibilities. US REITs alone hold $4.5 trillion in gross real estate assets as of 2024. That scale makes them one of the most significant vehicles in global capital markets. The role of REITs in property goes far beyond passive income. They reshape how capital flows into real estate, how markets price assets, and how individual investors build wealth alongside institutional players.

How do reits work in the property market?

REITs pool capital from thousands of investors to acquire and manage diversified property portfolios. A single REIT may own industrial warehouses, multifamily apartment complexes, medical office buildings, self-storage facilities, and hotels simultaneously. That breadth is what separates them from buying a single rental property.

The structural rule that defines every REIT is the dividend distribution requirement. REITs must distribute 90% of their taxable income to shareholders annually. This rule creates a reliable income stream for investors but limits the cash a REIT can reinvest internally. Growth must come from debt issuance or equity offerings instead.

The economic impact of REITs on the property market is substantial. US-listed equity REITs own nearly 570,000 properties, generate 3.6 million jobs, and contribute $283.4 billion in labor income annually. These numbers show that REITs are not just financial instruments. They are active participants in the physical real estate economy.

| Property Sector | Common REIT Examples | Investor Appeal |

|---|---|---|

| Industrial | Warehouses, logistics centers | E-commerce demand growth |

| Multifamily | Apartment complexes | Stable rental income |

| Healthcare | Medical offices, senior housing | Aging population tailwind |

| Self-Storage | Climate-controlled units | Recession-resistant demand |

| Hospitality | Hotels, resorts | Cyclical upside potential |

Pro Tip: When evaluating a REIT’s property mix, check whether its sectors are correlated. A REIT holding both hotels and retail faces compounded downside risk during economic contractions, while one mixing industrial and healthcare offers more natural balance.

What are the benefits of reits for real estate investors?

The benefits of REITs are most visible when you compare them directly to traditional property ownership. Buying a physical office building in Singapore or New York requires significant capital, active management, and tolerance for illiquidity. A REIT delivers exposure to the same asset class with none of those constraints.

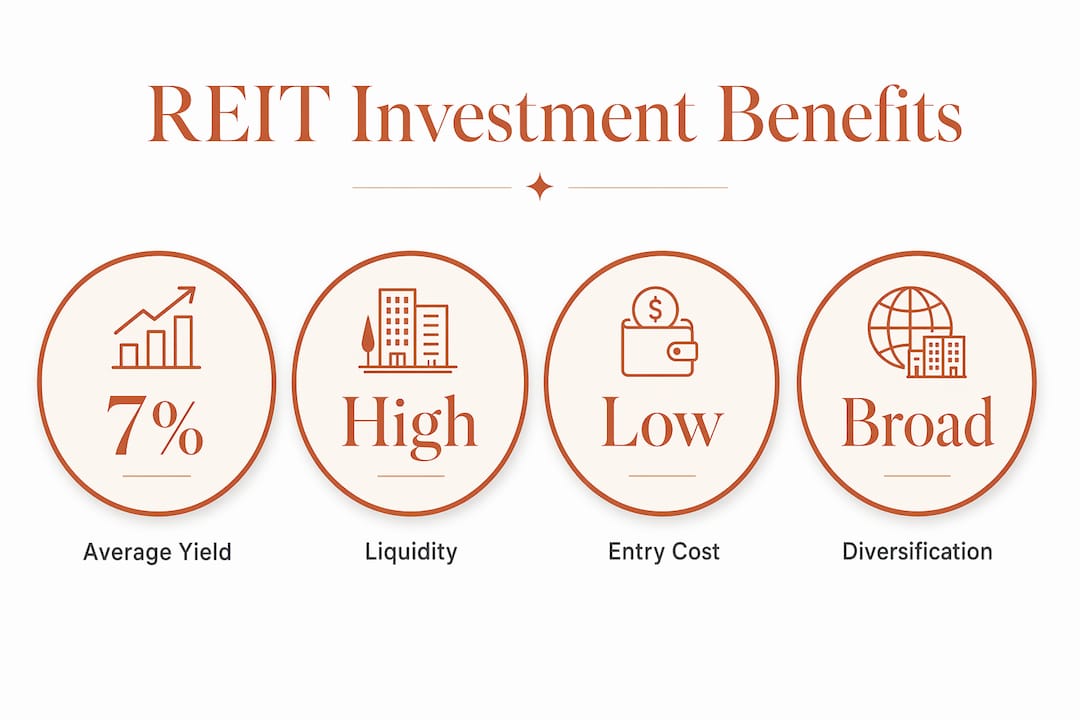

Liquidity is the most underrated advantage. Physical real estate can take months to sell. Publicly traded REITs trade on exchanges like the NYSE and SGX, meaning you can enter or exit a position in seconds. That flexibility matters when market conditions shift quickly.

Income generation is the second major draw. REIT dividend yields range between 3% and 8%, well above the S&P 500 average. Dividends have historically accounted for roughly 66% of long-term REIT total returns. That means the income component, not price appreciation, drives most of the wealth creation over time.

Diversification through REITs works on two levels. First, a single REIT gives you exposure to dozens or hundreds of properties. Second, diversification benefits extend across varied property types and geographic footprints, reducing the concentration risk that comes with owning one or two physical assets. For investors already holding direct property in Singapore, adding a US industrial REIT or a European logistics REIT through international property investment creates genuine geographic balance.

Lower capital barriers round out the advantages. You can buy into a REIT for the price of a single share, gaining access to institutional-quality assets that would otherwise require millions in direct investment.

Reits vs. traditional real estate: a direct comparison

| Factor | REITs | Direct Property Ownership |

|---|---|---|

| Liquidity | High (exchange-traded) | Low (months to sell) |

| Capital Required | Low (single share) | High (down payment + costs) |

| Management Burden | None | Active or outsourced |

| Diversification | Built-in | Concentrated |

| Dividend Income | 3%–8% yield | Rental yield varies |

| Tax Complexity | Moderate | High |

Key financial metrics for analyzing REIT investments

Net income is the wrong metric for evaluating a REIT. Real estate assets depreciate on paper under accounting rules, but physical properties often appreciate in value. That creates a distortion. Funds From Operations (FFO) corrects for this by adding depreciation back to net income, revealing the actual cash available for dividends. FFO is the standard metric used by REIT analysts at firms like Green Street Advisors and Nareit.

Leverage is the second critical variable. Because REITs cannot retain significant earnings due to mandatory distributions, they rely on debt and equity issuance to fund acquisitions. High leverage amplifies returns in rising markets but creates serious stress when interest rates climb or property values fall. Always check a REIT’s debt-to-equity ratio and interest coverage ratio before committing capital.

Tax structure adds another layer of complexity. Under US tax code, REITs must hold properties for at least two years to qualify for safe harbor treatment and avoid being classified as a dealer, which triggers higher tax penalties on property sales. This rule directly shapes how REIT managers time asset dispositions and portfolio rebalancing.

The risks specific to REITs include:

- Interest rate sensitivity. Rising rates increase borrowing costs and make REIT dividend yields less competitive against bonds.

- Sector cyclicality. Retail and hospitality REITs suffered severe dislocations during the 2008–2009 financial crisis and the COVID-19 bear market.

- Dilution risk. Frequent equity issuances to fund growth can dilute existing shareholders over time.

- Concentration risk. A REIT focused on a single geography or property type carries higher volatility than a diversified one.

REITs serve best as defensive income stabilizers and inflation hedges in a portfolio rather than long-term growth engines. Setting that expectation correctly prevents disappointment when a REIT underperforms high-growth equities during bull markets.

Pro Tip: Never evaluate a REIT on dividend yield alone. Always cross-check the payout ratio vs. cash flow to confirm the dividend is sustainable. A 9% yield backed by a 110% payout ratio is a warning sign, not an opportunity.

How to integrate reits into a property investment portfolio

Strategic allocation is where most investors get REITs wrong. They either ignore REITs entirely or overweight them chasing yield, without thinking about how they fit the broader portfolio.

Financial advisors recommend allocating 15%–30% of total investable assets to REITs, depending on income goals and risk tolerance. A retiree prioritizing stable income sits closer to 30%. A growth-focused investor in their 30s may hold 15% or less. The right number depends on your specific situation, not a generic rule.

Here is a practical framework for integrating REITs into a property-focused portfolio:

- Assess your existing real estate exposure. If you already own direct property in Singapore or elsewhere, your REIT allocation should complement rather than duplicate those holdings. Avoid stacking a Singapore commercial REIT on top of a physical commercial property in the same market.

- Select REITs by sector and geography. Use REITs to access sectors and markets you cannot reach through direct ownership. Industrial REITs in the US, data center REITs in Europe, and healthcare REITs in Asia each offer distinct return profiles. Understanding real estate asset management principles helps you evaluate how well a REIT’s management team executes on its portfolio.

- Hold REITs in tax-advantaged accounts where possible. REIT dividends are typically taxed as ordinary income. Holding them in an IRA, CPF Investment Scheme account, or equivalent tax-sheltered vehicle reduces the drag on net returns.

- Monitor leverage and REIT market cycles actively. Valuations become most attractive during market dislocations, as seen in 2008–2009 and during COVID-19. Investors who added exposure at those points captured significant re-rating gains as conditions normalized.

- Blend REITs with direct property for full-spectrum exposure. REITs provide liquidity and diversification. Direct ownership provides control, leverage, and tax benefits like depreciation. The two work better together than either does alone.

Pro Tip: Use rental property valuation methods to benchmark REIT-held assets against direct property in the same market. If a REIT’s implied cap rate is significantly lower than what you could achieve buying directly, that REIT may be overpriced.

Key takeaways

REITs are the most efficient vehicle for combining real estate income, diversification, and liquidity in a single investment structure.

| Point | Details |

|---|---|

| Core function | REITs pool investor capital to own income-producing properties across multiple sectors and geographies. |

| Income advantage | REIT dividends yield 3%–8% and account for roughly 66% of long-term total returns. |

| Right metric matters | Use FFO, not net income, to assess a REIT’s true distributable cash flow and dividend sustainability. |

| Allocation range | Allocate 15%–30% of investable assets to REITs based on income needs and risk tolerance. |

| Portfolio fit | REITs work best as income stabilizers and inflation hedges, not as substitutes for growth equities. |

What i’ve learned about reits after years in property markets

The biggest mistake I see investors make with REITs is treating them like a passive set-and-forget income product. They are not. REIT market performance dispersion is increasing as regional and sector nuances widen. A data center REIT in the US and a retail REIT in Southeast Asia are fundamentally different bets, even though both carry the REIT label.

My honest view is that most retail investors underestimate leverage risk. When interest rates rose sharply in 2022 and 2023, highly leveraged REITs saw their valuations compress far more than their underlying property values justified. The income looked safe on paper. The total return was ugly. Monitoring debt levels is not optional.

The investors I have seen do well with REITs treat them the way a good fund manager treats any asset: they select carefully, size positions deliberately, and rebalance when valuations stretch. They also combine REIT exposure with direct property holdings to capture benefits that neither vehicle delivers alone. That combination, done thoughtfully, is where real wealth progression happens.

— Aman

Build a stronger property portfolio with expert guidance

Understanding the role of REITs in property is one piece of a larger investment picture. Whether you are allocating capital across REITs, direct property, or both, the quality of your decisions depends on the quality of your market intelligence and advisory support.

At Aesthetic Havens, Aman Aboobucker and the ERA Realtors team work with investors across Singapore and international markets to identify high-performing assets, structure portfolios for income and growth, and navigate complex market conditions. From commercial property investment to full asset management strategy, the team brings the depth of analysis you need to make confident decisions. Reach out to discuss how REITs and direct property can work together in your portfolio.

FAQ

What is a REIT and how does it work?

A REIT is a company that owns or finances income-producing real estate and must distribute at least 90% of its taxable income to shareholders annually. Investors buy shares on public exchanges, gaining real estate exposure without direct property ownership.

How do reits differ from buying property directly?

REITs offer liquidity, built-in diversification, and low capital requirements, while direct property ownership provides control, leverage, and depreciation tax benefits. The two approaches complement each other in a balanced portfolio.

What financial metric should i use to evaluate a REIT?

Funds From Operations (FFO) is the standard metric because it adds depreciation back to net income, revealing the actual cash available for dividends. Net income alone understates REIT earnings due to large non-cash depreciation charges.

How much of my portfolio should be in reits?

Financial advisors recommend allocating 15%–30% of total investable assets to REITs, depending on your income goals and risk tolerance. Investors prioritizing stable income typically sit at the higher end of that range.

Are reits a good inflation hedge?

REITs provide a degree of inflation protection because property values and rents tend to rise with inflation over time. They work best as income stabilizers and inflation hedges rather than as primary growth vehicles in a portfolio.