Most Singapore landlords can tell you their monthly rent figure without hesitation. Far fewer can tell you what gross rental income actually includes under IRAS rules, or why confusing it with take-home cash flow is one of the most expensive mistakes a property investor can make. Understanding what is gross rental income goes well beyond knowing your monthly rent. It shapes how you file taxes, how you evaluate investment returns, and how accurately you forecast cash flow across a portfolio. This article breaks down the definition of rental income in Singapore, how to calculate it, what affects it, and how to use it to make smarter investment decisions.

Table of Contents

- What is gross rental income? Definition and components

- How to calculate gross rental income and its impact on Singapore tax

- Gross rental income vs. net rental income: Why the distinction matters

- Common pitfalls and advanced considerations in tracking gross rental income

- Practical application: Using gross rental income data for smarter property investment in Singapore

- Rethinking gross rental income: What most Singapore landlords overlook

- Enhance your investment strategy with expert real estate advisory in Singapore

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Gross rental income scope | Gross rental income includes rent, furniture charges, maintenance fees, and certain non-cash benefits under tenancy agreements. |

| Tax deductions options | IRAS allows a 15% deemed expense deduction plus mortgage interest or actual expenses when calculating taxable rental income. |

| Gross vs net income | Net rental income accounts for expenses and shows actual cash flow, providing a clearer investment profitability picture. |

| Common reporting pitfalls | Landlords often misclassify deposits and overlook vacancy prorating, understating true gross rental income by up to 10%. |

| Use data for strategy | Accurate gross rental income tracking enables better tax offsets, cash flow forecasts, and smarter investment decisions. |

What is gross rental income? Definition and components

Gross rental income is the total amount a tenant pays you, in any form, before you subtract any costs or expenses. Under Singapore’s tax framework, IRAS interprets rental income broadly under section 10(1)(f) to include non-cash benefits and payments due under tenancy agreements, not just cash received. That definition is wider than most landlords expect, and getting it right from the start saves you from under-reporting or over-claiming later.

Here is what counts as part of your gross rental income in Singapore:

- Monthly rent received from your tenant, including any rent paid in advance

- Furniture and fittings rent, if your tenant pays separately for the use of furnishings

- Maintenance fees or service charges paid by the tenant on your behalf

- Non-cash benefits, such as a tenant who renovates the property in exchange for reduced rent

- Lease premiums, meaning upfront lump sum payments for securing a tenancy

- Forfeited security deposits, but only once forfeited, not while held

What does NOT count? Refundable security deposits that you are holding but have not kept. These remain the tenant’s money until forfeiture. Understanding property leasing details in Singapore also matters here, since different lease structures can change what components show up in your gross income figure.

One often-overlooked point: if your tenant pays utilities or property tax directly to a third party on your behalf, that counts as income to you under IRAS rules. Even the reimbursement of costs is income. This is similar to how retail leasing definitions in commercial property treat tenant contributions as part of gross receipts. The principle is consistent across markets: if money flows because of your tenancy agreement, it is income.

How to calculate gross rental income and its impact on Singapore tax

Now that we know what gross rental income is, here is how to calculate it and understand its tax impact.

Calculating gross rental income is straightforward on the surface. Add up every payment you received from your tenant during the tax year that qualifies under the components listed above. That total is your gross rental income figure before any deductions.

Here is a simple example. Say you rent out a condominium unit in Singapore:

- Monthly rent: $3,500 x 12 months = $42,000

- Furniture rent: $200 x 12 months = $2,400

- Maintenance fees paid by tenant: $150 x 12 months = $1,800

- Total gross rental income = $46,200

From that gross figure, IRAS allows two options for deductions when calculating your taxable rental income:

- Option A (Deemed expense deduction): Deduct a flat 15% on gross rent for residential properties, plus actual mortgage interest. No receipts needed for the 15% portion since YA 2017. Simple and fast.

- Option B (Actual expense deduction): Claim real costs including property tax, agent fees, repairs, and insurance. You need receipts and documentation for everything.

You can also deduct mortgage interest under either method, which is a significant advantage for leveraged investors. One critical limitation: rental losses after expenses cannot offset your employment income or other income sources. They can only offset gains from other rental properties within the same year.

Pro Tip: If your property is relatively new and your actual expenses are low, the 15% deemed deduction often results in a larger deduction than your real costs. Run the numbers both ways before filing.

Accurate calculation also matters for calculating rental income and yield comparisons. Investors who understate gross income often also underestimate their yield, which skews their portfolio analysis.

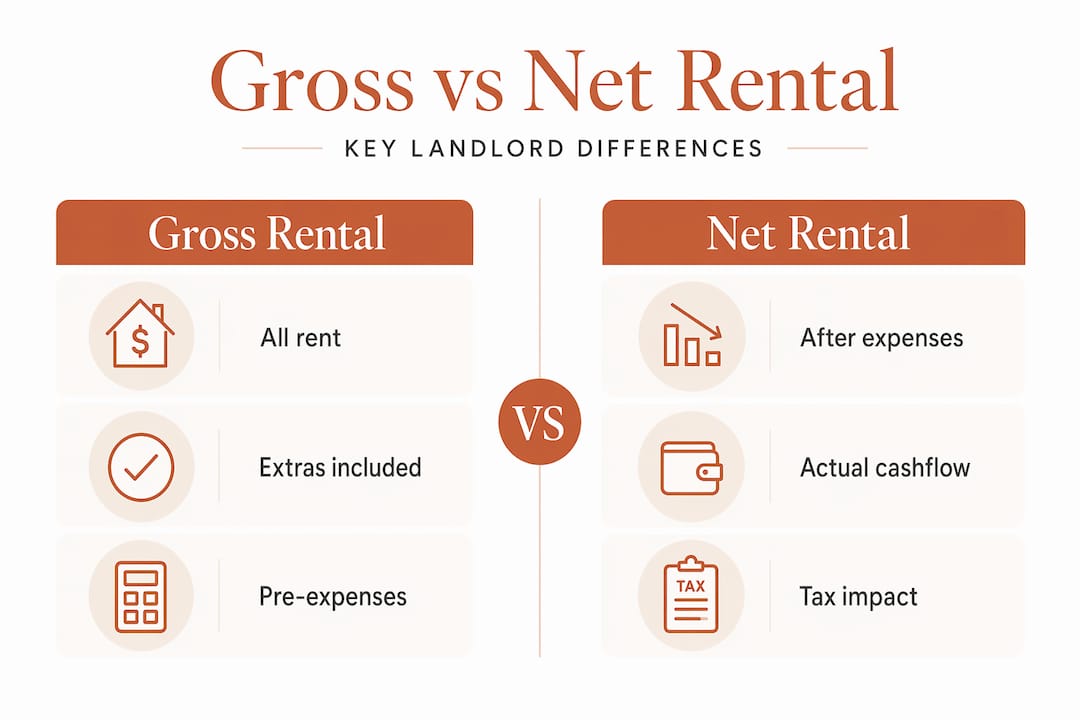

Gross rental income vs. net rental income: Why the distinction matters

Understanding the tax implications leads us to why gross and net rental incomes tell different investment stories.

Gross rental income is the headline number. Net rental income is the one that pays your bills. The definition of rental income in each case is the same, but what you subtract makes all the difference.

Here is a direct comparison using a Singapore residential property:

| Item | Gross rental income | Net rental income |

|---|---|---|

| Monthly rent + extras | $46,200/year | $46,200/year |

| Mortgage interest | Not deducted | ($18,000) |

| Property tax | Not deducted | ($3,500) |

| Agent and legal fees | Not deducted | ($2,400) |

| Maintenance and repairs | Not deducted | ($2,000) |

| Total | $46,200 | $20,300 |

That gap is not small. Net income in this example is less than half of gross. And Singapore’s high-cost market makes this gap sharper than in most other countries. The 1-2 percentage point gap between gross and net yield in Singapore significantly impacts cash flow for investors operating on thin margins.

Key differences to keep in mind:

- Gross income is used to calculate your taxable rental income starting point

- Net income tells you what you actually earn from the property

- Gross yield is useful for quick market comparisons between properties

- Net yield is the figure to use for investment decisions, financing, and cash flow planning

Pro Tip: Never evaluate a Singapore property purchase using gross yield alone. A property showing a 4% gross yield in a prime district can deliver below 2.5% net after factoring in property tax, sinking fund contributions, and agent fees. Always run the rental yield explained numbers to their net conclusion before committing.

Common pitfalls and advanced considerations in tracking gross rental income

With the basics clear, let us explore advanced nuances and common errors in gross rental income tracking.

Most landlords get the big numbers right. It is the edge cases that create problems at tax time and distort their investment analysis. Here are the most common ones:

- Security deposits held but not forfeited: These are not income yet. The moment your tenant forfeits the deposit (by breaking the lease or leaving the unit in poor condition), it becomes rental income in that tax year.

- Non-refundable lease premiums: Collected upfront and count as income immediately in the year received, not spread across the lease term.

- Early termination compensation: If a tenant pays you a sum to exit a lease early, that is rental income in the year you receive it.

- Vacancy prorating errors: If your property was vacant for three months, only nine months of potential rent applies. Many landlords overlook prorating for vacancies, understating true gross by 5-10% annually when doing investment comparisons.

The single most common mistake I see Singapore landlords make is treating a forfeited security deposit as a windfall rather than taxable income. IRAS expects it reported in the year of forfeiture, full stop.

For investors managing multiple units, these edge cases compound. Missing a forfeited deposit across three properties in the same year adds up to a material under-reporting of gross income. Staying on top of lease agreement nuances for each tenancy is not optional, it is a compliance issue.

Pro Tip: Create a simple tracker for each tenancy that logs the deposit amount, refund status, and any non-refundable premiums received. Update it at lease start, renewal, and termination. This takes 15 minutes and prevents hours of reconstruction at tax time. You can also explore value-adding investments that affect both the rent you can charge and the components that flow into gross income.

Practical application: Using gross rental income data for smarter property investment in Singapore

Finally, let us explore how to apply this knowledge to guide effective investment decisions and portfolio management.

Knowing your gross rental income precisely is not just about compliance. It is the raw data that drives everything from cash flow modeling to portfolio decisions. Here is how to use it well:

- Build property-level income statements. Track gross rental income separately for each unit you own. Accurate gross rental income per property is critical for offsetting rental losses across properties, so lumping everything together will cost you at tax time.

- Use gross income to compare market performance. Before expenses, gross yield lets you benchmark properties against each other and against the broader Singapore rental market.

- Model cash flow from net down, not gross up. Start with gross, subtract all foreseeable costs, and use the net figure to decide if the investment meets your cash flow requirements.

- Review annually, not just at tax time. Rent levels shift. Maintenance costs rise. An annual review of gross income against expenses reveals whether your yield is holding or eroding.

Pro Tip: Singapore’s rental market moved significantly in 2023 and 2024. If you have not repriced your properties and reassessed your gross vs. net income in the last 12 months, you may be working from outdated assumptions. Use market analysis strategies to ground your numbers in current data.

For investors managing a growing portfolio, gross income tracking also feeds directly into rental market insights that help you time acquisitions and disposals. The numbers you track today shape the decisions you make in year three and year five.

Rethinking gross rental income: What most Singapore landlords overlook

Here is the uncomfortable truth about how most Singapore landlords use the gross rental income figure: they treat it like a profit number. They see $46,000 a year in rent and think of that as their property’s return. It is not. It is the starting line.

Gross rental income is a measurement tool, not a performance indicator. The moment you start managing your property investments using gross income as the benchmark, you are flying blind on costs. And in Singapore’s high-cost property environment, costs are the variable that determines whether your investment is actually working for you.

What frustrates me most is that the information needed to go beyond gross income is entirely accessible. IRAS publishes clear guidance. Rental returns insights are available. The math is not complicated. The problem is habit. Landlords get anchored to gross rent because it is the figure they negotiate at lease signing. It feels definitive. It is not.

The landlords I see building durable property wealth in Singapore are the ones who track income at the net level from day one. They know their gross figures, yes. But they make every decision, from refinancing to renovation to selling, based on what the property actually puts in their pocket after all costs. That discipline is rare, and it is worth developing.

Is rental income taxable? Absolutely. And the gap between what you collect and what you keep after tax and expenses is the real story of your investment. Build your strategy around that gap, not around the headline rent figure.

Enhance your investment strategy with expert real estate advisory in Singapore

Navigating gross rental income calculations, tax implications, and portfolio strategy on your own is possible. Doing it optimally, without missing components or overpaying tax, is where professional advisory pays for itself.

At Aesthetic Havens, we work with Singapore property investors and landlords to build income tracking frameworks, evaluate gross and net returns accurately, and position portfolios for long-term yield growth. Whether you are managing a single condominium or a multi-property portfolio, understanding your income at every level is the foundation of a sound strategy. Our real estate advisory guide covers what to expect from professional advisory, and our insights on the commercial real estate market extend well beyond residential. When you are ready to invest with clarity, speak with a trusted Singapore realtor who understands both the numbers and the market.

Frequently asked questions

What exactly counts as gross rental income in Singapore?

Gross rental income includes all rent received, payments for furniture or maintenance charged to tenants, and non-cash benefits defined under tenancy agreements, excluding security deposits unless forfeited.

Can rental losses from one property offset income from my job or other sources?

No. Rental losses cannot offset employment or other income, but they can offset rental gains from other properties within the same tax year.

Why is net rental income more important than gross rental income for investors?

Net rental income accounts for mortgage interest, fees, and maintenance, giving you a realistic view of actual cash flow. The 1-2 percentage point gap between gross and net yield in Singapore’s market makes this distinction critical for any serious investor.

Are security deposits included in gross rental income?

Refundable security deposits are excluded from gross rental income until forfeited. Once a tenant forfeits the deposit, it counts as rental income in the year of forfeiture.

How can professional advisory services help with managing rental income?

Real estate advisory services provide expertise in tax strategies, income tracking, and market analysis to optimize rental income and investment returns in Singapore’s competitive property environment.