Stagnant rental returns despite rising costs are a frustration that far too many Singapore landlords know all too well. Your mortgage repayments climb, property tax assessments inch upward, and maintenance bills pile up, yet the rent you collect barely moves. The investors who consistently outperform are not simply luckier with their tenants. They rely on systematic, data-driven approaches that most landlords overlook entirely. This guide breaks down exactly how to benchmark, audit, optimize, and stress-test your rental portfolio using strategies that are specific to Singapore’s private residential market.

Table of Contents

- Know your benchmarks and calculate true rental yield

- Audit your property and area for yield potential

- Optimize cash flow: Control costs and increase rental value

- Stress-test your rental strategy for future resilience

- Beyond yield: Why resilient investors focus on risk-adjusted returns

- Work with experts to unlock your property’s full yield potential

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Benchmark with real data | Use official indices like URA PRPRPI to anchor rent pricing and target realistic yields. |

| Factor in net costs | Calculate net yield by including all recurring expenses, not just gross rent. |

| Audit your property features | Compare your unit with similar properties to identify value gaps and improvement opportunities. |

| Optimize for cost and value | Actively manage your cash flow and enhance unit appeal to boost returns. |

| Stress-test for resilience | Simulate adverse scenarios like higher rates and vacancies to ensure sustainable yields. |

Know your benchmarks and calculate true rental yield

Having set the stage for why a systematic approach matters, the first step is anchoring every decision in hard data rather than gut feeling.

Many landlords estimate what their unit should rent for based on what a neighbor told them at the last condo barbecue. That approach costs money. Singapore’s Urban Redevelopment Authority publishes the Private Residential Property Rental Price Index (PRPRPI), a quarterly index that tracks rental changes across the private residential segment using hedonic regression methodology. Hedonic regression isolates the effect of each property attribute, such as floor area, location, and floor level, so you are comparing like for like rather than mixing a renovated Orchard Road unit with an aging suburban apartment.

Using this index as your macro benchmark tells you whether the rental market is rising, plateauing, or contracting at the segment level. From there, you layer in property-level data to set a precise rent target. For a deeper breakdown of how these numbers translate into actual returns, see this guide on explaining rental yield in Singapore.

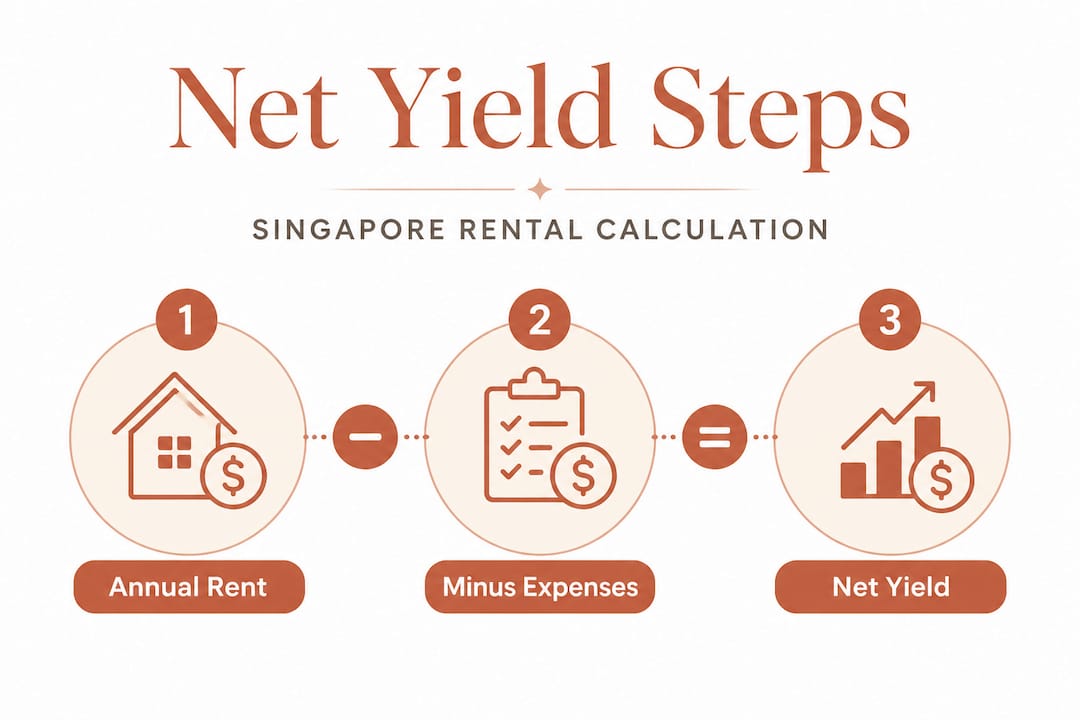

The single biggest mistake investors make is stopping at gross yield. Gross yield is simply annual rent divided by purchase price, expressed as a percentage. Net yield is what you actually keep. Here is a practical example:

| Item | Amount (SGD) |

|---|---|

| Monthly rent | $3,200 |

| Annual rental income | $38,400 |

| Annual mortgage repayment | $18,000 |

| Annual property tax | $2,400 |

| Annual maintenance and sinking fund | $3,600 |

| Annual insurance and misc. costs | $800 |

| Total annual expenses | $24,800 |

| Net annual income | $13,600 |

| Purchase price | $1,100,000 |

| Net yield | 1.24% |

A gross yield of 3.49% looks reasonable. A net yield of 1.24% demands immediate action. Knowing the difference is the foundation of every decision that follows. For a step-by-step walkthrough, this resource on understanding yield calculation is particularly useful.

Pro Tip: Build your net yield calculation in a simple spreadsheet and update it every quarter. Small cost increases compound fast, and catching them early gives you time to respond before they erode your returns significantly.

- Use the PRPRPI to track whether the private rental market is trending up or down at a macro level.

- Cross-reference with actual transacted rents, not asking prices, for your specific subzone.

- Include every recurring cost in your net yield formula: mortgage, property tax, management fees, and insurance.

- Review your calculation after any loan repricing, tax reassessment, or major repair.

Audit your property and area for yield potential

Once you understand your property’s numbers, the next step is to benchmark it against the competition and identify exactly where value gaps exist.

Not all units in the same development perform equally. A two-bedroom unit on a high floor with a pool view can command 15% to 20% more rent than an identical unit facing the carpark on a low floor. The discipline of using property-level comparables matched by age, size, and location is exactly what the hedonic methodology controls for. In practical terms, this means pulling URA rental transaction data and filtering for units within your development or directly comparable ones within 500 meters, then adjusting for floor, condition, and furnishing level.

Here is a comparison of typical gross yields by property type and location in Singapore’s private market:

| Property type | Area | Typical gross yield |

|---|---|---|

| Studio or 1-bedroom condo | Central Region | 3.0% to 4.2% |

| 2-bedroom condo | City Fringe (RCR) | 2.8% to 3.8% |

| 3-bedroom condo | Outside Central Region | 2.5% to 3.5% |

| Landed property | Various | 1.5% to 2.5% |

| HDB (subletting rooms) | Various | 4.0% to 6.0% |

Yields at the lower end of each band are typical for older, less well-located units or those with limited amenities. Yields at the upper end belong to units that tick the boxes tenants actually care about.

Here is a step-by-step property audit you can run yourself:

- List your unit’s current features: floor level, renovation year, furnishing quality, view, proximity to MRT, available storage, and car park access.

- Pull the top three comparable rentals in your development or within 500 meters that transacted in the last 90 days via URA’s rental transaction database.

- Score each feature as above, at, or below the comparable units on a simple grid.

- Identify your weakest two or three attributes and calculate the rental premium you are leaving on the table.

- Cross-reference with tenant demand trends in your subzone using the property leasing guide to understand which improvements move the needle most.

Pro Tip: MRT proximity is consistently the highest-value feature for expat and professional tenants in Singapore. A unit within a five-minute walk of an MRT station routinely commands a 10% to 15% rent premium over a comparable unit that is a 15-minute walk away.

Features that most influence tenant decision-making include renovated kitchens with modern appliances, updated bathrooms with good water pressure, fast and reliable Wi-Fi infrastructure, proximity to international schools for family tenants, and covered car parking. You can find detailed condo rental benchmarks that show exactly which amenity combinations attract the highest-paying tenant segments in each district.

Optimize cash flow: Control costs and increase rental value

With your yield potential mapped and your value gaps identified, the next move is taking concrete steps to limit expenses and simultaneously raise your rental income.

Cost control and revenue growth are two levers, and most landlords only pull one. Effective investors work both simultaneously. The four major expense categories eating into your net yield are mortgage repayments, property tax, maintenance, and vacancy-related income loss.

According to Singapore real estate market analysis, borrowing costs and operating expenses have risen to the point where net yields are being squeezed even when rents stabilize. This means cost management is no longer optional.

Cost control strategies that work:

- Refinance your mortgage: Even a 0.3% reduction in your home loan rate on a $1 million loan saves $3,000 annually. Check repricing windows every two to three years.

- Appeal your property tax: If your annual value assessment is inflated relative to current market rents, you can file a formal objection with IRAS. Many investors never do this and overpay for years.

- Preventive maintenance: A $150 servicing call for your air conditioning units prevents a $2,500 compressor replacement. Schedule quarterly checks and annual plumbing inspections.

- Shorten vacancy periods: Every month vacant on a $3,500 rent unit costs you $3,500. Engage an agent 60 days before your tenancy ends, not 10 days before.

Rental value enhancement strategies:

- Replace dated fixtures with modern fittings (budget $3,000 to $5,000) and target a $200 to $300 monthly rent increase.

- Add a washer-dryer combo if the unit lacks laundry facilities. This simple upgrade appeals strongly to professional and expat tenants.

- Market to rising tenant segments such as digital nomads, dual-income couples without children, and short-assignment corporate tenants.

- Offer flexible lease terms of six to 12 months if market conditions support it, which can justify a small rent premium.

Diversifying into other asset classes, such as understanding the benefits of commercial property, can also reduce your overall portfolio risk if residential yields tighten further. For a broader picture of where the market is heading, the latest Singapore rental market trends show which submarkets still offer meaningful upside.

Pro Tip: Do not renovate blindly. Survey three to five active tenants or agents operating in your subzone before spending. They will tell you exactly which features they get asked about and which ones tenants do not care about. This saves you from spending $10,000 on something that moves your rent by zero.

Stress-test your rental strategy for future resilience

After optimizing for the present, ensure your strategy stands up to shocks and uncertainty moving forward.

Most landlords build their rental investment model on today’s conditions and never revisit it. Interest rates change. Regulations shift. Tenants lose jobs. A strategy that looks solid in a stable market can collapse quickly when two or three variables move at once.

“It is not enough to calculate yield based on current conditions. The investors who survive market cycles are the ones who already know what happens to their cash flow when costs rise, rents fall, or vacancies extend. They have already run the numbers and prepared.” — Aman Aboobucker, Aesthetic Havens

Here is a step-by-step stress test you should run at least once a year:

- Identify your key variables: current interest rate, monthly rent, vacancy rate assumption, and total monthly expenses.

- Increase your loan interest rate by 1.5% to 2%: Calculate the new monthly repayment and determine how this changes your net cash flow. If your current rate is 3.5%, model at 5%.

- Simulate a two to three month vacancy: Remove two to three months of rental income from your annual total and recalculate net yield. Most investors are shocked by how quickly this turns positive cash flow negative.

- Apply a 10% rent reduction: Singapore rents have pulled back in certain submarkets. Model what happens if your tenant negotiates down or the market softens.

- Add a one-time repair cost of $5,000 to $8,000: Air conditioning, plumbing, or electrical issues happen. Factor in a realistic emergency maintenance event.

Once you have run these scenarios, the findings should drive real decisions. If a 2% rate increase and one month of vacancy puts you into negative cash flow, you need a larger financial buffer, a more conservative loan structure, or a diversified property portfolio. The property market trends for 2026 provide additional context on where stress points are most likely to emerge.

According to the Singapore real estate commentary, net yields are under pressure across the private residential segment as expenses rise faster than rents. Risk-adjusted thinking is no longer a nice-to-have. It is the core of a sound rental investment strategy.

Beyond yield: Why resilient investors focus on risk-adjusted returns

Here is the perspective most yield-chasing landlords need to hear: maximizing your headline rental yield is not the same as building real wealth from property.

We have worked with investors who owned units delivering 4% gross yields that were generating negative net cash flow once all real costs were factored in. They were so focused on the top-line number that they never calculated what they were actually keeping. Chasing the highest yield without accounting for risk is the property investment equivalent of driving fast in heavy fog. You feel like you are making progress until you are not.

Prudent investors in Singapore today do something different. They simulate stress scenarios before they buy, not after their cash flow breaks. They build three-month vacancy buffers into their financial planning. They prioritize tenant quality over marginally higher rent, because a reliable tenant who pays on time for three years is worth far more than a higher-paying tenant who leaves after eight months and requires two months of refurbishment.

The mental shift that separates resilient investors from frustrated landlords is moving from “what yield can I project?” to “what yield can I realistically keep, through rate cycles, soft markets, and unexpected costs?” That reframing changes everything from how you buy to how you manage. The market resilience analysis we track consistently shows that investors with diversified portfolios and adequate buffers outperform single-asset, maximum-leverage landlords over any five-year period.

Diversification across property types, building in cash flow buffers, and practicing adaptive leasing are not conservative moves. They are what allows you to hold through downturns and buy when others are forced to sell.

Work with experts to unlock your property’s full yield potential

Knowing the strategies is one thing. Executing them in Singapore’s fast-moving, regulation-heavy property market is another challenge entirely.

At Aesthetic Havens, we help landlords and investors do exactly what this guide describes: benchmark accurately, audit honestly, optimize deliberately, and plan with resilience. As a trusted Singapore realtor operating under ERA Realtors, Aman Aboobucker and the team bring data-driven market intelligence together with hands-on leasing expertise. Whether you need a full rental strategy review, help pricing your unit against current comparables, or want to explore whether your next investment should be residential or commercial, the leasing guide on our site is a strong starting point. For investors considering diversification, understanding the benefits of commercial property may open doors you have not yet considered.

Frequently asked questions

What is considered a good rental yield in Singapore?

A good gross rental yield for private residential property in Singapore typically ranges from 2% to 4%, though true net yield after expenses is usually meaningfully lower, as reflected in the URA rental index trends. HDB subletting arrangements can yield higher gross returns but come with separate regulatory conditions.

How do I calculate net rental yield for my Singapore property?

Net rental yield equals your annual rental income minus all annual expenses (mortgage, property tax, maintenance, insurance), divided by the purchase price, then multiplied by 100. The PRPRPI methodology helps you verify whether your rent target is realistic relative to current market conditions.

Why are net rental yields in Singapore under pressure lately?

Rising mortgage rates, higher property taxes, and climbing maintenance costs have outpaced rental growth for many private residential properties, and net yields are being squeezed even when headline rents remain stable. This makes cost control and cash flow stress-testing critical components of any landlord’s strategy.

Does upgrading my property always guarantee a higher rental yield?

Not automatically. Upgrades boost rental value only when they match what tenants in your specific subzone actively want. Research comparable rentals and consult active leasing agents before committing to renovation spending, since poorly targeted upgrades rarely recover their cost through higher rent.

Should I adjust my rental strategy during economic downturns?

Yes, and you should have your adjusted strategy ready before a downturn arrives, not during it. Stress-testing your cash flow in advance, with scenarios covering vacancy extensions and rate increases, lets you respond with a plan rather than react under financial pressure.