Most investors assume buying property in another country is just like buying domestically, only with a longer flight involved. That assumption gets expensive fast. What is cross-border property investment, really? It is the purchase of real estate in a country where you are not a resident or citizen, with all the legal, tax, financing, and currency complexity that brings. 37% of Canadians surveyed admitted they did not know enough about the cross-border buying process, and these are investors from a country that shares a border with the US. If knowledge gaps that wide exist there, they exist everywhere.

Table of Contents

- Key takeaways

- What cross-border property investment actually covers

- Legal and tax traps that catch investors off guard

- Financial realities: mortgages, cash, and currency risk

- How to actually execute a cross-border investment

- Popular markets compared

- My honest take on where most investors get this wrong

- How Aesthetic Havens can help you invest internationally

- FAQ

Key takeaways

| Point | Details |

|---|---|

| More than buying abroad | Cross-border property investment involves layered legal, tax, currency, and financing challenges beyond standard real estate. |

| Legal structuring is non-negotiable | Foreign ownership restrictions in many countries require trusts or special purpose vehicles decided before contract signing. |

| Currency risk runs deep | Exchange rate movements affect purchase cost, rental income, operating expenses, and exit proceeds simultaneously. |

| Local experts are your backbone | Success depends on coordinating brokers, tax advisors, and legal counsel across both home and target countries. |

| Exit planning starts at entry | Withholding taxes and compliance timelines must be factored in from day one, not when you decide to sell. |

What cross-border property investment actually covers

Cross-border real estate refers to any property transaction where the buyer and the asset exist in different legal jurisdictions. That covers more ground than most people expect.

The types of properties targeted vary considerably by investor profile:

- Residential properties such as condominiums, villas, and single-family homes are the most common entry point, often driven by lifestyle goals or rental income potential.

- Commercial real estate including offices, retail spaces, and logistics assets attracts institutional and experienced individual investors seeking yield.

- Development land and pre-construction projects appeal to investors looking for capital appreciation in emerging markets.

- Holiday or short-term rental properties in tourist destinations like Bali, the Costa Brava, or the south of France combine personal use with income potential.

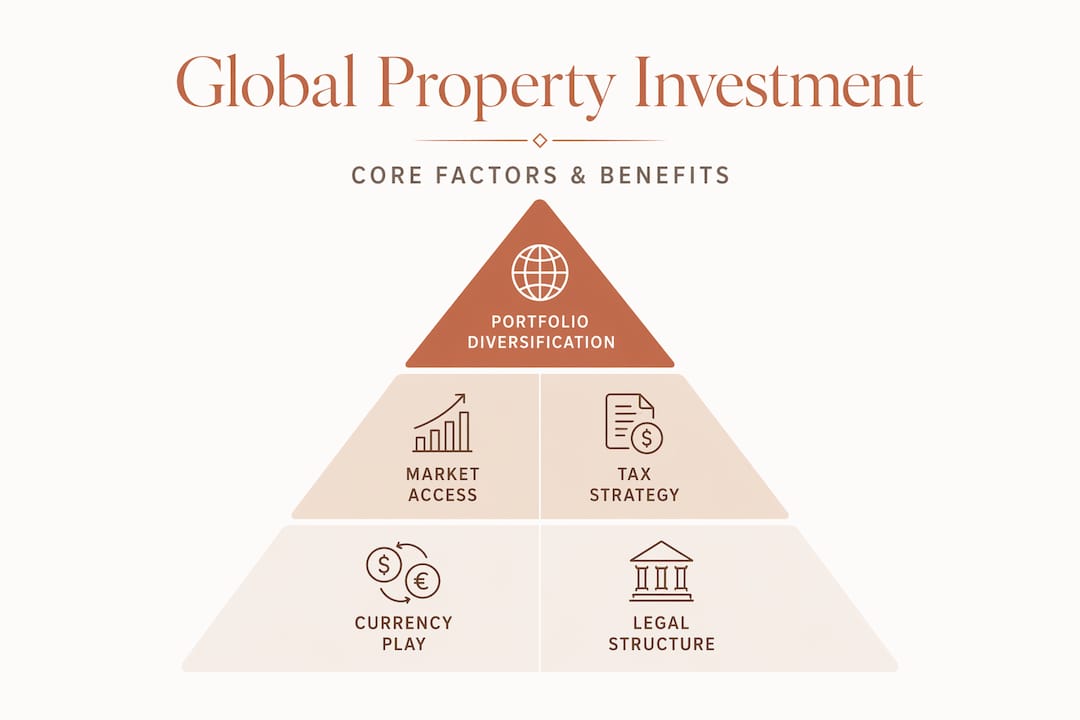

Investor motivations are equally diverse. Some buyers want portfolio diversification that reduces exposure to a single domestic market. Others pursue income generation in markets with higher rental yields than they can find at home. A third group is driven by lifestyle access, buying in places they love and want to retire to or visit regularly.

From a portfolio strategy perspective, international property investment sits in a unique category. It offers genuine non-correlation to domestic assets, since property cycles in Singapore, the US, and Portugal rarely move in lockstep. That diversification potential draws investors who want to manage single-market concentration risk, though it introduces a different set of management demands in return.

Legal and tax traps that catch investors off guard

This is where the gap between expectation and reality tends to be widest. The global property market is not a single system. Each country maintains its own rules on who can own property, under what structure, and what taxes apply on purchase, during ownership, and at exit.

Foreign ownership restrictions are one of the first obstacles. Mexico is a clear illustration. Foreign buyers in restricted zones, which include most coastal and border areas, cannot hold direct title. Instead, they must use a bank trust called a fideicomiso or a Mexican corporation. This is not optional. It is a legal requirement that must be resolved before the purchase contract is signed. Trying to sort out ownership structure mid-transaction leads to delays, renegotiation, and sometimes deal failure.

Tax obligations layer on top of ownership rules and operate across multiple jurisdictions simultaneously. When a Canadian resident sells a US property, FIRPTA withholds 15% of the gross sale price at closing. That is a cash-flow shock most first-time cross-border investors are not prepared for. Importantly, FIRPTA withholding is not a final tax. It is a mechanism. Reconciliation through tax filing is required to recover any excess, but that process takes time and requires competent US tax counsel.

Double taxation treaties complicate things further. Most developed countries have bilateral tax treaties that determine which country has primary taxing rights on rental income and capital gains, but the specifics vary enormously. Singapore investors buying in the UK operate under different treaty provisions than those buying in Japan or Australia.

Pro Tip: Engage a tax advisor in both your home country and the target country before you sign anything. The cost of dual advisory is small compared to the tax liability of getting the structure wrong from day one.

Legal structuring tools such as trusts, special purpose vehicles (SPVs), and holding companies are used to manage ownership compliance, liability, and succession planning. The decision on ownership structure should happen at the research stage, not after an offer is accepted. Changing structure mid-transaction in many jurisdictions triggers additional stamp duty, registration fees, or approval delays.

Financial realities: mortgages, cash, and currency risk

Most investors discovering the global property market for the first time assume that mortgage financing works the same way abroad as it does at home. It does not, and this has significant consequences for how you structure a deal.

US-style 30-year fixed-rate mortgages are not a globally available product. In most European, Asian, and Latin American markets, mortgages for foreigners either do not exist or come with variable rates, shorter terms, and substantial down payment requirements. Many cross-border investors end up relying on cash purchases or seeking specialized cross-border lenders.

The layers of currency exposure

Currency risk is not a single number. It operates at multiple points across the investment lifecycle, each affecting deal economics differently:

| Exposure point | What it affects | Risk direction |

|---|---|---|

| Purchase | Entry cost in home currency | Rate moves before funds transfer |

| Operating costs | Maintenance, taxes, management fees | Ongoing exchange rate volatility |

| Rental income | Monthly cash flow converted home | Weakening target currency reduces yield |

| Financing | Loan servicing if borrowing in foreign currency | Adverse moves increase debt burden |

| Exit proceeds | Net sale value in home currency | Rate at exit can swing net return significantly |

Currency movements affect every one of these layers simultaneously, and they can move in opposite directions. A property that earns a 6% gross yield in its local market might return 3.5% or 8% to you in Singapore dollars depending on exchange rate shifts over five years. This is why currency exposure modeling alongside property fundamentals is not optional but a core part of the analysis.

Pro Tip: Run your deal model at three exchange rate scenarios: current rate, a 10% adverse shift, and a 20% adverse shift. If the 20% scenario still meets your minimum return threshold, you have a genuinely resilient investment.

The financing strategy and currency plan need to be designed together. Borrowing in the target currency hedges some currency risk but introduces local interest rate exposure. Borrowing in your home currency is simpler but leaves full currency exposure on the asset side.

How to actually execute a cross-border investment

Understanding the principles is one thing. Getting a transaction completed across borders, with remote management afterward, requires a systematic approach.

- Market research first, enthusiasm second. Research the macroeconomic fundamentals, rental demand, vacancy rates, and price history of your target market before visiting. Emotional attachment to a location is a liability in investment decision-making.

- Map the legal and tax environment early. Understand foreign ownership rules, required structures, and both-country tax obligations before engaging with specific properties. This shapes which investment structures are even available to you.

- Assemble your cross-border team. You need a local real estate broker who specializes in foreign buyers, a legal advisor in the target country, a tax advisor who understands cross-border obligations in both jurisdictions, and a currency specialist if large transfers are involved.

- Secure financing clarity before making offers. Know whether you are buying cash, using local financing, or leveraging a home-country facility. Mortgage availability abroad is often limited for foreign nationals, so financing certainty protects you from being unable to close.

- Plan the operational structure before closing. Managing international money transfers, setting up local banking, organizing property management, and accounting for rental income all need to be in place before you take ownership, not discovered as problems afterward.

- Build your exit strategy into the entry plan. Know your FIRPTA obligations, your capital gains tax exposure in the target country, and your treaty protections before buying. The cost of an unplanned exit is almost always higher than the cost of proper upfront structuring.

For investors exploring Singapore’s role as a base or target market, the foreigners’ guide to Singapore property covers the specific regulatory and tax framework that applies in 2025.

Popular markets compared

The investment opportunities overseas vary dramatically by region in terms of legal accessibility, tax treatment, and market characteristics.

| Market | Ownership restrictions | Key tax issue | Typical investor profile | Market outlook |

|---|---|---|---|---|

| United States | Largely open to foreigners | FIRPTA withholding at exit | Income-focused, capital growth | Stable, deep market |

| Singapore | Foreigners restricted on landed property | ABSD applies to foreign buyers | Regional HNW investors, long-term holders | Strong, regulated |

| Mexico (coastal) | Fideicomiso or SPV required | Capital gains tax on sale | Lifestyle buyers, short-term rental investors | Growing tourism demand |

| Portugal | Open to EU and non-EU buyers | NHR tax regime available | Retirees, EU residency seekers | Competitive, high demand |

| Thailand | Foreigners cannot own land directly | Withholding and transfer taxes | Condo buyers, retirees | Active but legally restricted |

Southeast Asia as a region shows some of the most active cross-border real estate flows, but also some of the most complex ownership rules. Singapore remains one of the more structured and transparent markets, which is part of its appeal to cross-border investors seeking stability even with its higher entry costs and foreign buyer stamp duties.

Europe offers relatively open ownership structures for non-EU investors in most markets, with Portugal’s tax regimes and Spain’s coastal markets attracting consistent attention. The US remains the dominant destination for cross-border capital due to market depth and diversification value, despite the FIRPTA complexity at exit.

My honest take on where most investors get this wrong

In my experience advising clients on international property investment, the mistakes that cost the most money are almost never the obvious ones. Investors do their research on the property itself, the location, the developer, the yield projections. What they skip is the financial modeling work that should sit underneath all of that.

Currency risk is the most consistently underestimated factor I see. Clients will spend hours analyzing local rental yields and then build their financial model entirely in the target country’s currency. When I ask them to rerun the numbers in Singapore dollars at a 15% adverse exchange rate, the deal often looks dramatically different. The property has not changed. The risk was always there.

Legal structuring is the other area where I see people cut corners on cost and then pay multiples of that saving in complications. I have seen investors who decided to handle ownership structure “later” and had to renegotiate the entire purchase agreement after exchanging contracts. The legal fee to set up the right structure upfront is always smaller than the cost of fixing a wrong one.

My honest advice: treat cross-border investing like you are running a small business in a foreign country, because you essentially are. You need the right team, a conservative financial plan, and the discipline to plan for the exit before you sign on entry. The returns can be genuinely strong. But they go to investors who respect the complexity, not those who assume it away.

— Aman

How Aesthetic Havens can help you invest internationally

Thinking about expanding your real estate portfolio beyond Singapore? That is exactly where working with Aesthetic Havens makes a material difference. Aman and the team at Aesthetic Havens specialize in guiding investors through both Singapore and international property markets, coordinating legal, tax, and financing considerations across jurisdictions so you do not have to figure it out alone.

Whether you are a first-time cross-border buyer or an experienced investor looking to diversify into new markets, Aesthetic Havens provides real estate advisory tailored to your specific financial goals and risk profile. From identifying the right market to structuring your ownership and managing compliance, the guidance you get is practical, specific, and experience-backed. Reach out directly to start with a no-obligation consultation.

FAQ

What is cross-border property investment?

Cross-border property investment is the purchase of real estate in a country where the buyer is not a resident or citizen. It involves navigating foreign ownership laws, multi-jurisdiction tax obligations, currency risk, and international financing.

Can foreigners own property in any country?

No. Many countries restrict foreign ownership or require specific legal structures. Mexico requires a bank trust or corporation for coastal zone purchases, Thailand prohibits foreigners from owning land directly, and Singapore restricts foreigners from buying landed residential property.

How does FIRPTA affect cross-border investors?

When a foreign national sells US property, FIRPTA withholds 15% of the gross sale price at closing. This is not the final tax owed. Investors must file a US tax return to reconcile the withheld amount and recover any excess.

Why is currency risk so significant in international property investment?

Currency exposure operates across every stage of ownership: purchase price, operating costs, rental income, loan servicing, and exit proceeds. A property earning strong local yields can still deliver poor returns in the investor’s home currency if the exchange rate shifts adversely during the holding period.

Do I need a local expert when buying property abroad?

Yes, and ideally more than one. You need a local broker who works with foreign buyers, a legal advisor in the target country, and a tax advisor who understands obligations in both your home country and the target market. Managing cross-border transactions without local professional support is one of the most common and costly mistakes investors make.