Most people think property financing is simply about getting a loan. It is not. The role of property financing goes far deeper than securing funds to close a deal. It shapes your cash flow, determines which properties you can realistically pursue, and either supports or undermines your long-term wealth goals. In Singapore’s tightly regulated market, where LTV caps, TDSR limits, and MSR rules all interact at once, understanding how mortgage financing truly works is the difference between a deal that performs and one that quietly drains you.

Table of Contents

- Key Takeaways

- The role of property financing: Singapore’s core rules

- How financing fits residential, investment, and commercial deals

- How loan structure shapes your returns

- HDB loans, bank loans, and commercial financing compared

- Applying financing knowledge to your own decisions

- My perspective: financing is the deal within the deal

- Ready to structure your property financing properly?

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Financing is a wealth strategy | Treat loan structure as a long-term financial decision, not just a means to purchase property. |

| Three caps control your loan | Singapore applies LTV, TDSR, and MSR simultaneously; your eligible loan is the lowest of all three. |

| Property type changes financing rules | Residential, investment, and commercial properties each require different financing structures and carry different risks. |

| Loan structure shapes returns | Interest rates, tenure, and amortization directly affect monthly cash flow and total investment performance. |

| Early planning prevents surprises | Model your full affordability before committing to a property to avoid underfunding at the worst moment. |

The role of property financing: Singapore’s core rules

Before you can use financing strategically, you need to understand the rules governing it. Singapore’s regulatory framework for property loans is more layered than most buyers expect.

Three metrics control your borrowing power simultaneously:

- Loan-to-Value (LTV): The maximum loan amount as a percentage of the property’s purchase price or valuation. For a first residential property with a loan tenure within the limits, LTV caps reduce leverage, requiring buyers to fund more in cash or CPF as tightening since 2013 has deliberately curbed investment-driven borrowing.

- Total Debt Servicing Ratio (TDSR): The TDSR is capped at 55% of your gross monthly income, meaning the total monthly repayments on all your debt obligations cannot exceed that threshold.

- Mortgage Servicing Ratio (MSR): If you are buying an HDB flat or Executive Condominium still under the Minimum Occupation Period, an additional MSR cap of 30% applies on top of the TDSR, further constraining what you can borrow.

The critical insight most buyers miss is this: your actual loan eligibility is the lowest of all three caps applied together. Focusing only on LTV gives you a false sense of how much you can borrow. Experienced Singapore buyers apply all caps in an integrated model to avoid being surprised at loan approval.

| Metric | What it controls | Who it affects most |

|---|---|---|

| LTV | Max loan as % of property price | All buyers and investors |

| TDSR | Monthly debt as % of gross income | Anyone with existing loans |

| MSR | Mortgage payment as % of gross income | HDB flat and EC buyers only |

For small business owners, this gets more complex. Business income is assessed differently from employment income, and existing business debts may count against your TDSR. Consulting a Singapore mortgage guide before committing to any property purchase is not optional. It is the step that keeps deals from falling apart at the financing stage.

How financing fits residential, investment, and commercial deals

The purpose of your property changes everything about how financing works and what it costs you.

Buying a home to live in

For owner-occupiers, the priority is affordability and stability. The goal is to secure a loan you can comfortably repay while building equity over time. The importance of property loans here is straightforward: without them, most buyers simply cannot enter the market at all. But the structure of that loan, the tenure, rate type, and monthly repayment, directly affects your quality of life for the next 25 years.

Buying an investment or rental property

Here, the calculus shifts entirely. Financing decisions impact monthly debt service and cash flows, which determines whether the property generates a surplus or a deficit each month. Two investors buying identical units can produce entirely different returns based on their loan terms alone. One investor with a shorter tenure and higher rate might see negative monthly cash flow, while another with a longer tenure and lower blended rate turns a profit from day one.

Pro Tip: When evaluating an investment property, calculate your debt service coverage before signing anything. Divide your projected monthly rental income by your monthly loan repayment. A ratio below 1.0 means the rent does not cover the mortgage, and you will be funding the gap from your own pocket.

For property investment strategies built around portfolio growth, each financing decision also affects your ability to borrow for the next property. Using maximum leverage on the first deal may feel smart, but it can lock you out of future opportunities.

Commercial property acquisitions

Commercial financing is a different world. Commercial real estate uses a layered capital stack where senior debt typically covers 60 to 75% of the loan-to-cost ratio, with mezzanine debt or preferred equity filling the gap between senior debt and the owner’s equity. Construction loans are short-term instruments, usually 12 to 36 months, with monthly interest payments on draws, and they convert to permanent financing once the project stabilizes. Understanding these layers is not just technical knowledge. It is fundamental to knowing whether your commercial project is even viable before you commit capital.

How loan structure shapes your returns

This is where the benefits of real estate financing become concrete and measurable.

Your loan’s structure determines:

- Monthly cash flow — The difference between a 20-year and 30-year tenure on a $1.5 million loan at 3.5% is roughly $2,000 per month. That gap can be the difference between a profitable rental property and a loss-making one.

- Total interest cost — A longer tenure reduces monthly payments but significantly increases the total interest paid over the loan’s life. The right choice depends on your income, other investment goals, and portfolio timeline.

- Flexibility for refinancing — Loan structure influences refinancing options and overall investment success. Loans with tight lock-in periods or high early redemption penalties can trap you in unfavorable rates when market conditions change.

- Risk exposure — Over-leveraging is the most common mistake in property investment. If rental income drops or interest rates rise, an over-leveraged investor faces repayment pressure with no buffer.

“Mortgage and real estate financing should be treated as a strategic long-term wealth decision. The structure of your loan influences not just what you pay today, but what you can do with your wealth tomorrow.” — Real estate financing strategy

Refinancing deserves more attention than most buyers give it. Many Singapore borrowers lock into a rate, forget about it, and miss the window to refinance when better rates become available. Building a review cycle into your property ownership routine, perhaps every two to three years, is one of the lowest-effort ways to protect your returns. Smart real estate wealth decisions consistently treat refinancing as part of the strategy, not an afterthought.

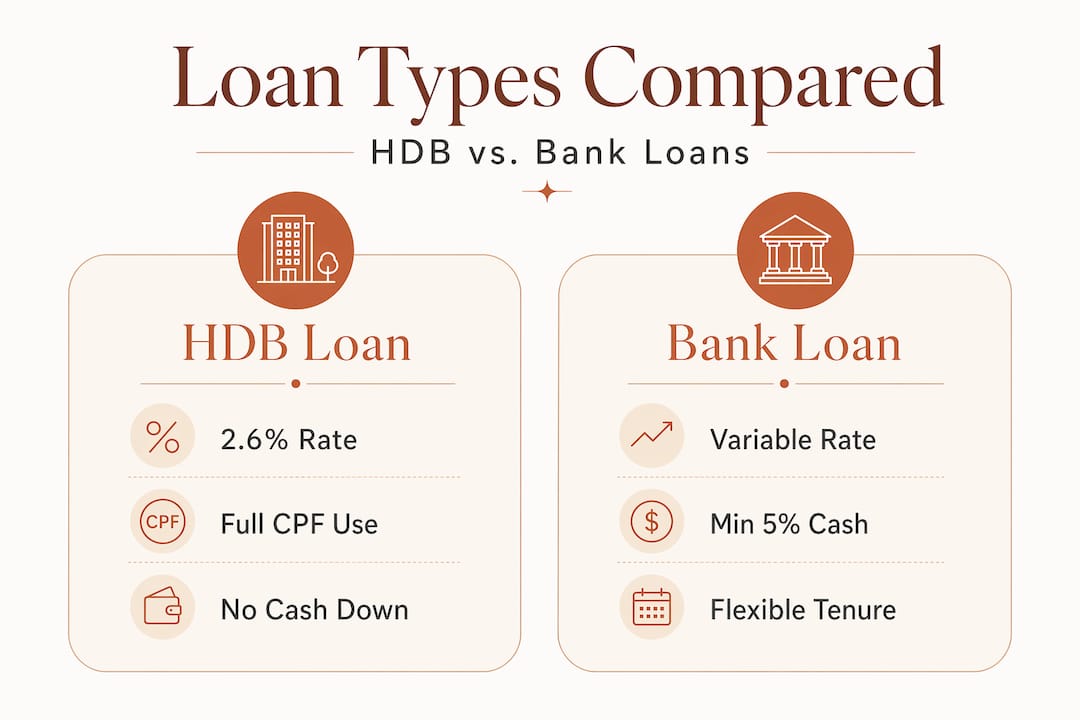

HDB loans, bank loans, and commercial financing compared

Singapore buyers face a specific choice when financing residential property: the HDB concessionary loan or a bank loan.

| Feature | HDB loan | Bank loan |

|---|---|---|

| Maximum LTV | 75% | 75% |

| Interest rate | Fixed at 2.6% | Variable (typically 3.0 to 3.8%) |

| Cash down payment | None required (full CPF allowed) | Minimum 5% cash required |

| Flexibility | Less flexible, no lock-in penalty | Lock-in periods with early redemption fees |

| Best for | Cash-constrained buyers | Buyers seeking rate flexibility |

HDB concessionary loans allow the full CPF Ordinary Account balance to cover the down payment, making them accessible for buyers with limited cash savings. Bank loans require at least 5% cash down regardless of CPF balance, but they offer lower initial rates and greater flexibility for buyers who plan to refinance.

The right choice depends on your income stability, cash reserves, and how long you plan to hold the property. HDB loans are forgiving. Bank loans are cheaper in favorable rate environments but carry more risk when rates move against you.

For commercial property, the mechanics are more complex. Business owners acquiring shophouses or commercial units should understand commercial property acquisition processes, including how construction loans work during the development phase. Monitoring monthly draw schedules and interest reserves is not the developer’s problem alone. Owners in joint ventures or development projects need to track loan conversion timing or risk liquidity problems that derail the entire project.

Pro Tip: For commercial financing, ask your lender at the outset exactly when the construction loan converts to permanent financing and what conditions trigger that conversion. Delays can leave you paying higher short-term rates for longer than projected.

Applying financing knowledge to your own decisions

Knowing how property financing works is one thing. Applying it to your specific situation requires a structured process.

- Start with your TDSR and MSR. Before looking at any property, calculate your current total monthly debt obligations and compare them to 55% of your gross income. This tells you your maximum additional loan repayment capacity.

- Run an LTV scenario. Based on the property type and whether it is your first or subsequent loan, determine the maximum LTV available to you, then calculate the resulting cash and CPF required upfront.

- Model multiple loan tenures. Do not just pick the maximum tenure. Model a 20-year and 25-year option side by side to see the monthly cash flow and total cost difference.

- Ask about lock-in periods and penalties. Some bank packages look attractive but impose 1.5% early redemption fees within the first two to three years. If you plan to sell or refinance, this matters enormously.

- Build a cash buffer. Beyond the down payment, you need stamp duty, legal fees, and three to six months of mortgage payments in reserve. Underfunding the purchase is one of the most common and preventable mistakes.

- Revisit your financing every two years. Markets change, rates change, and your income changes. Reviewing your loan structure regularly is part of managing property as a wealth asset.

For buyers with foreign income or those buying under commercial entities, the eligibility rules are more specific. A guide for foreigners buying property in Singapore covers the additional TDSR and financing restrictions that apply.

My perspective: financing is the deal within the deal

I have worked with enough buyers and investors to see a clear pattern. The ones who struggle are almost never undone by the property itself. They are undone by the financing they arranged around it.

I have seen clients choose a property they loved, then accept whatever loan terms were offered because they were focused on the unit, not the structure. Six months later, they are cash-flow negative and wondering why the investment is not working. The property was fine. The financing was wrong.

What I have learned is that how you finance a property matters as much as what you buy. Two clients can own identical units in the same development and have completely different financial outcomes based purely on their loan decisions. One structures for cash flow. The other maximizes leverage. The first builds steadily. The second stresses every time rates move.

The most overlooked part of financing is the refinancing window. Most buyers treat the loan as a one-time decision. In practice, your rate environment two years from now might be meaningfully better or worse, and your ability to act on that depends entirely on how you structured things at the start. Lock-in periods, redemption penalties, and partial prepayment options are not fine print. They are strategic levers.

My advice: before you calculate what property you can afford, calculate what loan structure serves your actual goals. The two are not the same question.

— Aman

Ready to structure your property financing properly?

Financing decisions made without expert context can cost you significantly over the life of a property. At Aesthetic Havens, we work with residential buyers and business owners across Singapore to align property selection with the right financing approach from the start.

Whether you are purchasing your first HDB flat, expanding an investment portfolio, or acquiring commercial space, our advisory approach accounts for your full financial picture. Understanding what real estate advisory actually involves can change how you approach every financing and property decision you make. We also cover investment property management so your financing strategy connects directly to your rental income goals. Reach out to Aesthetic Havens for a consultation that goes beyond the loan form.

FAQ

What is the role of property financing in Singapore?

Property financing provides the capital needed to purchase residential, investment, or commercial property while structuring repayment terms that affect cash flow and long-term wealth. In Singapore, it operates within strict regulatory limits including LTV, TDSR, and MSR caps that collectively determine your actual borrowing power.

How does TDSR affect my property loan eligibility?

The TDSR cap of 55% of gross monthly income limits the total monthly repayments across all your debts, meaning existing car loans, personal loans, or business debt reduce what you can borrow for property. For HDB flats, the additional MSR cap of 30% further restricts the mortgage repayment portion specifically.

What is the difference between an HDB loan and a bank loan?

HDB concessionary loans offer a fixed 2.6% rate with no cash down payment required, while bank loans require at least 5% cash down but offer potentially lower variable rates and greater refinancing flexibility. The right choice depends on your cash reserves, rate outlook, and how long you plan to hold the property.

How does financing structure affect investment property returns?

Loan tenure, interest rate, and monthly repayment amount directly determine whether a rental property generates positive or negative cash flow each month. Different financing structures can produce materially different investment returns for properties with identical purchase prices and rental income.

When should I consider refinancing my property loan?

Reviewing your loan every two to three years is a practical approach, particularly when your lock-in period expires or when market rates drop significantly below your current rate. Refinancing at the right time can reduce monthly payments and lower total interest cost over the remaining loan tenure.

Recommended

- How to Buy Commercial Property in Singapore: A Step-by-Step Guide | Aesthetic Havens

- Property leasing in Singapore: A complete 2026 guide

- Foreigner’s Guide to Buying Property in Singapore (2025 Regulations & Taxes) | Aesthetic Havens

- Why invest in Singapore property? Growth, stability, and opportunity