Most people assume that buying a property means owning it forever. In Singapore, that assumption can cost you dearly. The truth is that leasehold ownership gives you the right to occupy a property for a fixed period, after which the land reverts to the State. And here is the part that surprises most buyers: the overwhelming majority of homes in Singapore, from HDB flats to private condominiums, fall under this category. Understanding what leasehold actually means, how it shapes your property’s value over time, and what it means for your financing options is not optional knowledge. It is essential.

Table of Contents

- What is leasehold property? Clarifying the basics

- Singapore HDB and private leaseholds: How tenure affects ownership

- Leasehold property value decay: Bala’s Table and market realities

- Investor and buyer strategies: Risks, financing, and holding period

- The uncomfortable truth most buyers miss about Singapore leaseholds

- Expert help for leasehold decisions: Connect with property advisors

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Leasehold is time-limited | Buying leasehold means you own property only for the lease term, not indefinitely. |

| Check remaining lease | Always verify how many years are left before buying, as this affects price and financing. |

| Value decay framework | Use Bala’s Table and market insights to understand how property value declines over time. |

| Investor strategy matters | Smart buyers focus on holding period, resale liquidity, and financing—not just headline tenure. |

| Expert support available | Real estate advisors and agents can help you navigate leasehold decisions effectively. |

What is leasehold property? Clarifying the basics

Leasehold property refers to a title where you own the unit for a specific, defined period. Think of it less like buying a house outright and more like purchasing a very long tenancy with ownership rights during that period. Once the lease runs out, your right to occupy and use the property ends, and the land returns to the State.

In Singapore, the most common leasehold duration is 99 years. However, you will also encounter 60-year and even 999-year leaseholds in the market. The 999-year variety is sometimes called “near-freehold” because, in practical terms, it behaves very similarly to owning the land forever. The key distinction lies in how tenure, transfer rights, and long-term value differ between leasehold and freehold.

Here is a clear comparison to anchor your understanding:

| Feature | Freehold | 99-year leasehold | 999-year leasehold |

|---|---|---|---|

| Ownership duration | Indefinite | 99 years from grant | 999 years from grant |

| Land reverts to State? | No | Yes, at expiry | Yes, but practically distant |

| Resale value trajectory | Generally stable | Declines as lease shortens | Mostly stable |

| Typical price premium | Higher | Lower entry cost | Moderate premium |

| Financing restrictions | Fewer | Increases with age | Very few |

| Common property types | Landed, some condos | HDB, most condos | Older shophouses, some condos |

When it comes to property leasing in Singapore, leasehold properties dominate the landscape simply because the Singapore government retains land ownership and grants leases rather than selling land outright in most cases. Freehold land is genuinely scarce, which is why freehold condos typically command a significant price premium.

Key distinctions buyers should keep in mind:

- Freehold means you own the property and the land it sits on with no expiry date

- 99-year leasehold is the standard for HDB and most private residential developments

- 999-year leasehold was common in older developments and colonial-era grants

- The lease clock starts from the date the State grants the lease, not when you purchase the unit

- A 20-year-old 99-year leasehold property already has only 79 years remaining on its lease

Singapore HDB and private leaseholds: How tenure affects ownership

All HDB flats are 99-year leasehold properties, which means every single public housing unit in Singapore is subject to a lease expiry. This is a fundamental reality that many first-time buyers overlook, especially when purchasing resale flats.

Here is what makes this particularly important: the lease clock does not start ticking when you buy the flat. It starts when the block was completed or when the HDB originally granted the lease. So if you purchase a resale flat that was built in 1990, you are not buying a fresh 99-year lease. You are buying a property with roughly 63 years remaining as of 2026, not 99.

This distinction has real consequences across several dimensions:

- CPF usage restrictions. The government restricts how much CPF (Central Provident Fund) savings you can use to purchase a resale flat based on the remaining lease. If the remaining lease does not cover the youngest buyer to age 95, CPF usage is prorated.

- HDB loan eligibility. HDB loans require the remaining lease to cover the youngest buyer to at least age 80, or financing eligibility is reduced.

- Bank loan restrictions. Private bank loans become harder to secure as the remaining lease shortens, and loan-to-value ratios may be reduced.

- Resale liquidity. Flats with shorter remaining leases attract fewer buyers, which compresses prices and makes them harder to sell.

- Future en bloc potential. Some leasehold private condos may qualify for collective sale (en bloc), which can deliver windfall gains to owners before the lease gets too short.

“For Singapore’s public housing, all HDB flats are 99-year leasehold, so the lease term affects resale and financing over time.” The practical implication is that two flats in the same block can have meaningfully different financial profiles depending on when they were sold to their current owners.

Pro Tip: Before committing to any resale HDB flat or older private leasehold condo, always confirm the remaining lease years from official documents, not the headline “99-year” figure in the listing. A quick check on the HDB Resale Portal or the title deed can save you from a financing surprise later.

For buyers considering condo rental deals as a stepping stone before purchasing, understanding how remaining lease affects rental yield is equally important. A property with a shorter remaining lease may rent well today but could lose resale value faster than anticipated. Understanding your condo downpayment requirements in the context of a leasehold property is also essential before you commit any capital. You can explore rental pricing options to benchmark what comparable properties command in the current market.

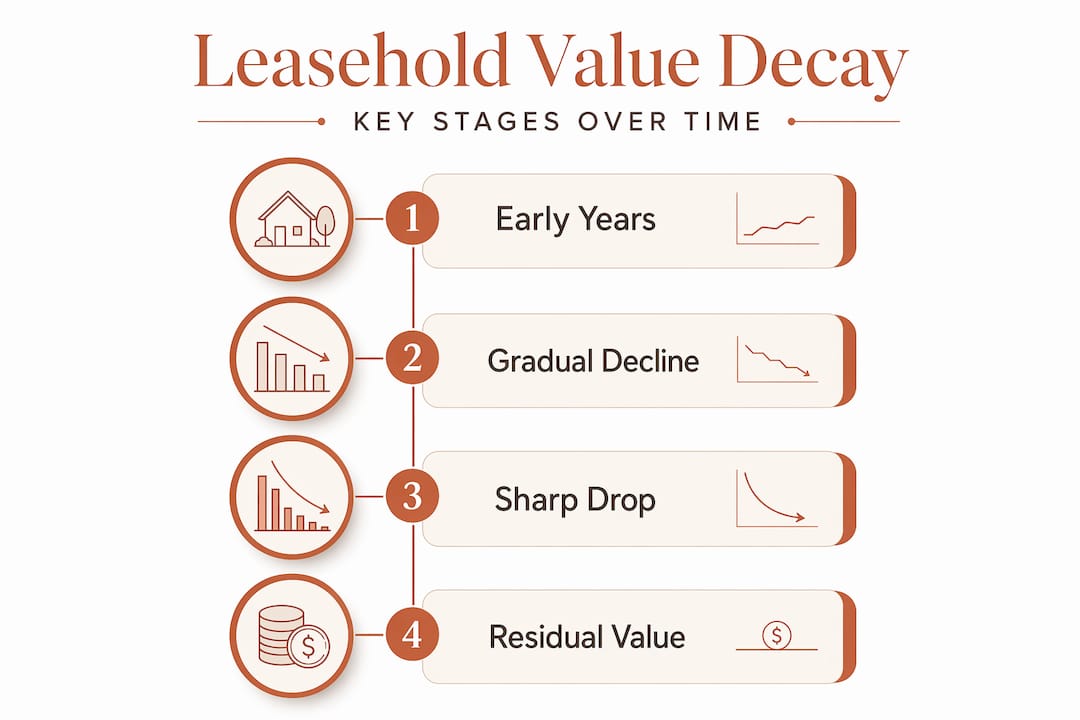

Leasehold property value decay: Bala’s Table and market realities

As a leasehold property’s remaining tenure shortens, its value does not decline in a straight line. It follows a curve that accelerates in the final decades. This is where Bala’s Table becomes an important concept for anyone serious about leasehold property in Singapore.

Bala’s Table is a leasehold relativity and valuation framework used in Singapore to model how a property’s value decays relative to its remaining lease. It essentially assigns a percentage of freehold value to a leasehold property based on how many years remain on the lease. The curve shows gradual decline in the early decades, then steeper decline as the lease drops below 60 years, and a sharp drop when it falls below 30 years.

Key insights from Bala’s Table benchmarks:

- A property with 99 years remaining might be valued at close to 100% of its freehold equivalent

- At 60 years remaining, the value drops to roughly 80% of freehold equivalent

- At 30 years remaining, the value could fall to around 50% or lower

- Below 30 years, the property becomes very difficult to finance and nearly impossible to sell at a reasonable price

However, real-world market behavior does not always follow Bala’s Table perfectly. Location, property condition, nearby amenities, and broader market sentiment all influence actual transaction prices. During bull markets, even aging leasehold properties in prime districts have held value better than the table predicts. During downturns, the decay can be faster than theory suggests.

The important takeaway from property evaluation benchmarks used across markets is that leasehold valuation is never purely mechanical. It requires judgment, market awareness, and timing.

For those looking at commercial real estate as an alternative, leasehold risk is equally present but often analyzed with different frameworks tied to income yields rather than capital appreciation. Understanding the benefits of commercial property can help you decide whether a shift from residential leasehold to commercial makes sense for your portfolio.

“Bala’s Table is a structured benchmark, though it may not fully match secondary-market behavior,” which means buyers should treat it as a guide, not a guaranteed prediction of resale outcomes.

Pro Tip: When comparing two leasehold properties, always calculate the “value per remaining lease year” rather than just comparing headline prices. A property that appears cheaper may actually be more expensive per year of ownership when you factor in the remaining tenure.

Investor and buyer strategies: Risks, financing, and holding period

Here is the reality that separates sophisticated property investors from casual buyers: the debate between leasehold and freehold is not just about sentiment or preference. It is fundamentally a question of time, liquidity risk, and financing conditions.

The leasehold vs. freehold decision is about your remaining lease, your planned holding period, and whether you can exit comfortably before the lease reaches a threshold that restricts financing or kills resale demand. These three factors matter far more than the headline tenure figure.

Here is a practical framework for evaluating any leasehold property as an investor or buyer:

- Calculate the remaining lease at purchase. Do not work backward from the original 99 years. Find out the actual grant date and subtract.

- Define your holding horizon. Are you buying to live in for 10 years? Hold for rental income for 20 years? The right remaining lease depends entirely on your exit timeline.

- Model your exit lease figure. If you buy a property with 70 years remaining and hold for 15 years, you will be selling a property with 55 years remaining. Is that still financeable and sellable?

- Check CPF and bank financing rules now. Do not assume today’s policies will stay the same. Tighter rules over time have consistently made shorter-lease properties harder to finance.

- Factor in en bloc potential. Older leasehold private condos with less than 70 years remaining can attract en bloc bids if the land value justifies redevelopment. This is a genuine upside worth researching.

For most buyers, the sweet spot is a leasehold property with at least 70 to 80 years remaining, which gives enough runway for a 15 to 20 year holding period before financing restrictions start to bite on the resale end.

On the 999-year leasehold question: banks and valuers treat these almost identically to freehold properties for financing and valuation purposes, even though technically they are still leasehold. In practice, if you are choosing between a 999-year leasehold and a true freehold of comparable location and condition, the 999-year property is usually the better value buy since freehold commands a price premium that may not fully justify the near-identical practical benefits.

Pro Tip: If you are buying a leasehold property primarily for rental income and plan to hold it for fewer than 15 years, remaining lease becomes less critical than yield, tenant demand, and location. But if capital appreciation and a clean exit are important to you, prioritize remaining lease years above almost everything else.

Understanding your responsibilities as a landlord in leasing arrangements also affects how you should think about leasehold investments. For overseas buyers, our foreigners’ buying guide walks through specific restrictions that apply when purchasing leasehold properties in Singapore. You can also explore rental lead management tools to maximize occupancy rates while you hold your leasehold investment.

The uncomfortable truth most buyers miss about Singapore leaseholds

Most buyers fixate on the headline tenure number as if 99 years sounds like an eternity and therefore the issue can be ignored. It cannot. The real risk in leasehold property is not about whether you personally run out of lease years. Almost no owner does. The risk is about liquidity and exit conditions at the point when you need to sell.

A property with 55 years remaining is not just worth less than one with 80 years remaining. It is fundamentally harder to sell. Fewer buyers can finance it. CPF usage is restricted. Bank loan tenors are compressed. The pool of potential buyers shrinks dramatically, and that compression in demand directly suppresses the price you can achieve.

What most buyers also miss is that this risk is asymmetric. The first 30 to 40 years of a 99-year leasehold, the value holds up reasonably well and follows the broader market. But once you cross into 60 years remaining territory, the decay accelerates, and the liquidity squeeze becomes a real problem for sellers.

The most practical guidance we can offer is this: buy leasehold with full awareness of your exit, not just your entry. Always check your leasing rights and obligations before committing, and seriously consider reading our breakdown of why Singapore property remains a strong investment even within leasehold structures.

The 999-year leasehold case also deserves a revisit. Buyers sometimes dismiss these properties because “leasehold” sounds inferior. But when banks treat them as near-freehold and they are priced below true freehold, they can represent genuine value if the location is strong.

Expert help for leasehold decisions: Connect with property advisors

Navigating leasehold choices requires more than reading guides. It requires someone who can assess your specific situation, your holding horizon, your financing profile, and your exit strategy, and match that to the right property at the right remaining lease.

At Aesthetic Havens, we specialize in exactly this kind of advisory work. Whether you are a first-time buyer trying to understand why two similar flats have such different price tags, or an investor building a portfolio across multiple asset classes, our team is here to help. Our real estate advisory guide explains the full scope of how professional advisory works in Singapore. You can also learn more about what real estate agents do and how they protect your interests in a leasehold transaction. Connect with us directly at Aesthetic Havens to speak with a licensed advisor who understands the leasehold landscape in Singapore.

Frequently asked questions

What happens when the lease of a property expires in Singapore?

When the lease expires, ownership reverts to the State and occupants no longer have any legal right to remain on the property. In practice, most leasehold properties are redeveloped or acquired by the government well before the lease actually reaches zero.

How do I check the remaining lease of a property before buying?

For private properties, check the title deed through the Singapore Land Authority. For HDB flats, verify via the HDB portal or the flat’s official lease documentation, not the listing description.

Can HDB flats with less than 60 years of lease be financed easily?

Financing becomes significantly harder as the remaining lease shortens, with banks imposing lower loan-to-value ratios and CPF usage becoming restricted based on the buyer’s age and the property’s remaining tenure.

Is a 999-year leasehold property in Singapore similar to freehold?

For most financing and valuation purposes, 999-year leaseholds are treated as functionally equivalent to freehold, though they remain technically leasehold and will eventually revert to the State.

How does Bala’s Table help in valuing leasehold properties?

Bala’s Table provides a structured leasehold valuation benchmark by assigning a percentage of freehold value based on remaining lease years, though actual market prices can diverge from these theoretical figures based on location and demand.