Two condos sit side by side in Jurong East. Same size, same age, same street. Yet one investor pockets 3.8% annually while the other struggles to clear 2.1%. What explains the gap? Property yield. This single metric tells you how hard your money is working relative to what you paid for the property. Most Singapore investors track price trends and loan eligibility but gloss over yield mechanics, and that gap quietly costs them thousands each year. This article breaks down what property yield means, how to calculate it accurately, where Singapore stands globally, and exactly how you can push your returns higher.

Table of Contents

- What is property yield?

- How to calculate property yield: Singapore examples

- Benchmarking property yield: Singapore vs. global markets

- Factors affecting property yield and how to improve it

- Common mistakes and pitfalls in property yield analysis

- Why property yield isn’t the whole story in Singapore

- Get expert help for your Singapore property investments

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Yield definition matters | Knowing how property yield is calculated helps you compare investments confidently. |

| Benchmarks vary by area | Singapore yields are generally lower but more stable than many markets, so set your expectations accordingly. |

| Optimization is possible | You can boost yields by selecting the right unit type, managing costs, and reducing vacancy time. |

| Avoid common errors | Always account for all expenses and use realistic estimates to avoid costly mistakes in yield analysis. |

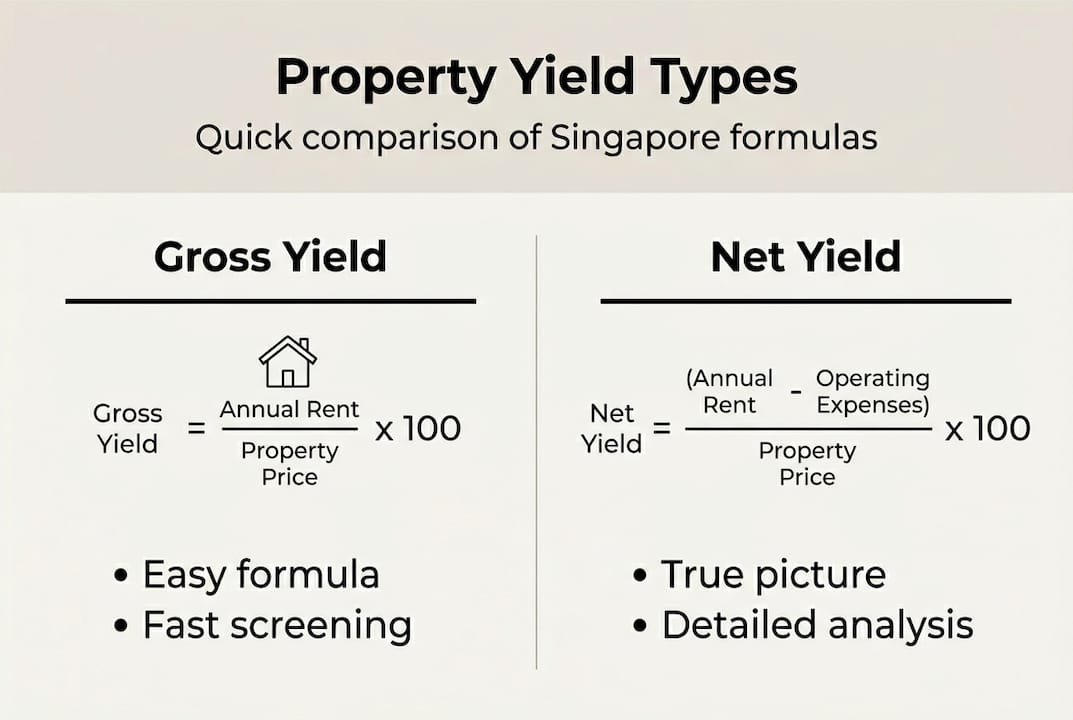

What is property yield?

Property yield is the ratio of your annual rental income to the value of your property, expressed as a percentage. Think of it as a report card for your investment. A higher percentage means your asset is generating more income relative to its cost. As covered in rental yield explained, understanding what yield measures and why it matters is the foundation every Singapore investor needs before making any purchase decision.

There are two types you need to know:

- Gross yield: Annual rental income divided by property price, multiplied by 100. Simple, fast, and useful for quick comparisons.

- Net yield: Annual rental income minus all expenses, divided by property price, multiplied by 100. This is the number that actually reflects what lands in your pocket.

Gross yield is easy to calculate from a listing page, but it flatters the investment. Net yield gives you the real picture. Understanding property yield basics is what separates investors who make informed decisions from those who overpay for underperforming assets.

| Metric | Formula | Best used for |

|---|---|---|

| Gross yield | (Annual rent ÷ Property price) × 100 | Quick screening |

| Net yield | ((Annual rent – Expenses) ÷ Property price) × 100 | Accurate return analysis |

Yield also functions as a comparison tool across property types, neighborhoods, and even countries. A 3% yield on a $1.5 million condo tells you something very different from a 3% yield on a $400,000 HDB flat, once you factor in expenses, risk, and liquidity.

Pro Tip: Always calculate both gross and net yield for every property you evaluate. Use gross for fast filtering, and net for your final decision.

How to calculate property yield: Singapore examples

Seeing the formulas in action removes all ambiguity. Here is how to apply them using two common Singapore property scenarios. As outlined in our mortgages and affordability guide, your financing costs interact directly with yield, so getting the calculation right from the start matters.

Step-by-step process:

- Find your annual rental income (monthly rent × 12).

- List all annual expenses: maintenance fees, property tax, insurance, management fees, repairs, and estimated vacancy loss.

- Apply the gross yield formula: (Annual rent ÷ Purchase price) × 100.

- Subtract total expenses from annual rent, then divide by purchase price and multiply by 100 for net yield.

- Compare your result against Singapore benchmarks to assess performance.

Practical Singapore examples using current Singapore rental yield data:

| Item | Suburban condo ($1.2M) | HDB flat ($500K) |

|---|---|---|

| Monthly rent | $3,200 | $2,100 |

| Annual rent | $38,400 | $25,200 |

| Annual expenses | $9,600 | $4,800 |

| Gross yield | 3.20% | 5.04% |

| Net yield | 2.40% | 4.08% |

The HDB flat delivers a significantly higher yield in this example. That surprises many investors who assume condos are the stronger performers. The reality is that lower entry prices and modest expenses can produce better income ratios, even if the absolute rent is lower.

Pro Tip: Vacancy loss is often forgotten. Budget at least 4 to 6 weeks of empty tenancy per year when calculating net yield, especially in a competitive rental market.

Benchmarking property yield: Singapore vs. global markets

Knowing your yield number is only meaningful when you can compare it to something. How does Singapore actually stack up against the rest of the world?

Typical yields in Singapore range from 2% to 4% for private condos, with smaller suburban units occasionally clearing 4.5%. That may sound modest compared to global alternatives, but context is everything. Singapore yields are modest by international standards, yet they come with a level of market stability, legal clarity, and tenant quality that most higher-yield markets simply cannot offer.

| Market | Typical gross yield | Stability rating |

|---|---|---|

| Singapore | 2% to 4% | Very high |

| Australia | 3% to 5% | High |

| United Kingdom | 4% to 7% | Moderate |

| United States | 5% to 9% | Moderate to variable |

| Hong Kong | 2% to 3% | Moderate |

“Investors who focus exclusively on yield often miss the fuller picture. In Singapore, professional property management and targeting smaller units in well-connected suburbs can consistently push yields toward the upper end of the range.”

Singapore’s regulatory environment, including the Singapore cooling measures that shape demand and pricing, intentionally suppresses speculative behavior. That keeps yields anchored but also protects capital values. It is a deliberate trade-off. Markets like the US or UK may offer 6% or 7% gross yields, but vacancy risk, property management complexity, and currency exposure erode that advantage quickly.

For investors considering diversification beyond residential, commercial property trends in Singapore are showing interesting yield movements in 2026, and commercial property benefits can complement a residential yield strategy well.

Factors affecting property yield and how to improve it

Yield is not fixed. Several levers are entirely within your control, and understanding them separates passive investors from those who consistently outperform the market. Key levers for optimizing yields include property size, location, and vacancy management, but the list goes deeper than that.

Here are the major variables that shape your yield:

- Location: Proximity to MRT stations, schools, and employment hubs drives rental demand and supports stable pricing.

- Property type and size: Smaller units command proportionally higher rents relative to purchase price, boosting yield percentages.

- Purchase price: Overpaying at acquisition permanently compresses your yield ceiling, no matter how well you manage the property afterward.

- Vacancy rate: Every month a unit sits empty erodes your annual income. Tenant quality and lease timing matter enormously.

- Management fees: Full-service property management typically costs 8% to 12% of monthly rent, which directly reduces net yield.

- Cooling measures and loan limits: Government restrictions affect how much leverage you can deploy, shaping your effective cost of capital.

Actionable moves to improve your net yield:

- Target undervalued neighborhoods with strong rental pipelines rather than already-popular districts where entry prices are inflated.

- Use a property investment guide to evaluate each purchase against both yield and capital growth potential before committing.

- Renegotiate management fees annually and compare providers to avoid paying above-market rates.

- Stage lease renewals to avoid simultaneous vacancies across a portfolio.

Pro Tip: Use expert yield tips to analyze rental demand data by subzone before purchasing. Areas with a high ratio of renters to available units sustain stronger yields over time.

Common mistakes and pitfalls in property yield analysis

Even investors who understand the formulas regularly make errors that quietly damage their actual returns. Knowing the traps is half the battle.

- Using gross yield as a final answer. Gross yield is a starting point, not a conclusion. Net yield after all expenses is what you actually earn. Many investors compare gross figures across properties and end up choosing worse-performing assets.

- Overestimating rental income. Basing projections on peak market rents rather than sustainable median rents inflates your yield forecast. Use verified rental transaction data, not asking prices from listing portals.

- Ignoring renovation and refresh cycles. Every 5 to 7 years, most rental units need meaningful upgrading to stay competitive. Failing to budget for this crushes your long-term net yield.

- Treating high yield as automatic validation. As noted in Singapore yield explained, a high yield figure can sometimes signal elevated risk, low capital growth potential, or a declining location rather than a superior investment.

- Missing hidden costs. Sinking fund contributions, ad-hoc special levies for condo facilities, and short-term vacancy between tenancies are costs that critical mistakes in yield calculations often go overlooked until they appear on a statement.

Pro Tip: Build a simple annual yield tracker in a spreadsheet that updates your net yield each quarter as actual expenses come in. This keeps your real return visible and identifies cost blowouts early.

Why property yield isn’t the whole story in Singapore

Here is something most yield-focused articles will not tell you: obsessing over yield can actually lead you to worse investments in Singapore specifically.

We have worked with investors who chased 4.5% suburban yields and ignored prime district condos yielding 2.8%. Five years later, the prime asset had appreciated 30% while the suburban unit barely moved. The total return, including capital growth, was not even close.

Singapore is unusual. The government actively manages housing supply, foreign demand, and land scarcity. These forces push capital appreciation in premium locations at rates that dwarf yield differences. Checking the rental market challenges of any given year shows how quickly supply and demand shift.

The right approach is to match your yield target to your personal objective. If you need monthly income, prioritize net yield. If you are building long-term wealth, weight capital growth more heavily. Never copy another investor’s benchmark without understanding their time horizon and goals. Yield is a tool, not a verdict.

Get expert help for your Singapore property investments

Understanding property yield is a genuine advantage. Acting on it effectively requires current market intelligence, access to verified rental data, and someone who knows which buildings and districts consistently outperform.

At Aesthetic Havens, we help Singapore investors move from calculation to confident decision. Whether you are evaluating your first rental property or optimizing a growing portfolio, our team under ERA Realtors brings real transaction experience to every advisory session. Explore 2026 property opportunities shaping Singapore’s market, or connect with us directly through Aesthetic Havens for a personalized yield analysis and investment review tailored to your goals.

Frequently asked questions

What is a good property yield in Singapore?

A good gross property yield in Singapore typically falls between 2% and 4%, with smaller suburban units occasionally reaching higher. Singapore yields of 2% to 4% reflect the market’s stability and regulatory environment rather than underperformance.

How is property yield different from capital appreciation?

Yield measures annual rental income as a percentage of property price, while capital appreciation tracks the increase in the property’s market value over time. As explained in yield versus appreciation, both metrics together form a complete picture of investment return.

How do I improve my property’s net yield?

Reducing expenses, minimizing vacancy periods, and choosing properties in areas with strong rental demand are the most direct levers. Strategies to improve yield by managing costs and vacancy consistently produce better net returns without requiring a new purchase.

Are high-yield properties always better investments?

Not always. High yields can sometimes signal higher risk, weaker capital growth, or a less desirable location. Balancing high yield versus growth potential is essential for making well-rounded investment decisions in Singapore.

Recommended

- Rental Yield Explained: Boost Your Singapore Property Returns

- Unlocking Value: The Top 5 Undervalued Singapore Neighbourhoods for Property Investment in 2025 | Aesthetic Havens

- Top benefits of investing in commercial property in Singapore

- The Ultimate Guide to Smarter Singapore Property Investments in 2025 | Aesthetic Havens