Singapore’s executive condominium is genuinely misunderstood. Most buyers assume it’s just a cheaper private condo with extra red tape. The real picture is more interesting: the EC scheme serves Singaporeans who earn too much for HDB flats but find fully private condos out of reach. That hybrid positioning gives ECs a pricing structure, an appreciation profile, and a lifestyle offer that private condos simply cannot replicate at the same entry price. If you’re seriously weighing your next property move, understanding why buy executive condo matters now more than ever, especially with major policy changes reshaping the market in 2026.

Table of Contents

- Key takeaways

- Why ECs cost less than private condos

- Lifestyle and community benefits

- Ownership rules and the 2026 MOP changes

- Investment considerations and long-term value

- Financial planning and the buying process

- My perspective on ECs in 2026

- How Aesthetic Havens can guide your EC purchase

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Price advantage is real | New ECs launch 25-30% below comparable private condos, letting you buy more space for the same budget. |

| Investment returns are strong | Historical data shows ECs appreciate 40-60% over 10 years, outpacing private condos in comparable periods. |

| New MOP rules change planning | The Minimum Occupation Period extended to 10 years from May 2026, requiring a longer commitment from buyers. |

| Financing limits matter | The Mortgage Servicing Ratio caps monthly repayments at 30% of gross income and often restricts borrowing more than the LTV ratio does. |

| Location determines outcomes | Capital appreciation depends heavily on project location, entry price, and proximity to upcoming infrastructure like new MRT lines. |

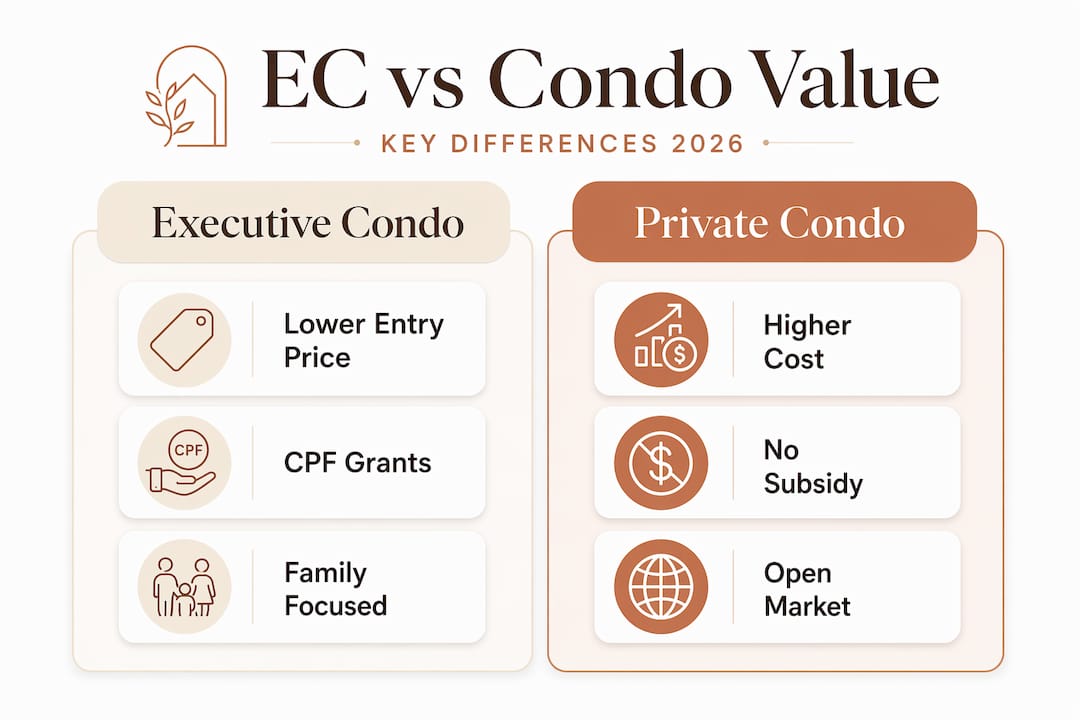

Why ECs cost less than private condos

The price gap between executive condominiums and private condos is not marginal. Suburban private condos currently transact at S$2,000 to S$2,100 per square foot, while new EC launches price at S$1,400 to S$1,500 per square foot. That is a 25 to 30% discount on a per-square-foot basis. On a 1,200 square foot unit, the difference can easily exceed S$700,000.

This pricing gap exists because ECs receive government land subsidies and are developed under Housing and Development Board regulations during the initial ownership period. For buyers, this subsidy translates directly into purchase savings, not just lower sticker prices.

The benefits of executive condos go beyond the base price. First-time buyers can tap CPF Family Grants of up to S$30,000, which further reduce the effective purchase cost. Then there is the progressive payment scheme. Rather than paying the full purchase price upon signing, buyers pay in staged construction milestones across three to four years, which reduces early cash flow pressure significantly.

Here is a quick snapshot of how the numbers compare for a similar 1,200 sq ft unit:

| Specification | Executive Condo | Suburban Private Condo |

|---|---|---|

| Price per sq ft (2026) | S$1,400 to S$1,500 | S$2,000 to S$2,100 |

| Total unit price (approx.) | S$1.68M to S$1.80M | S$2.40M to S$2.52M |

| CPF grant eligibility | Yes (first-timers) | No |

| Progressive payment | Yes | Yes |

| Buyer restriction | Singapore Citizens/PRs | Open market |

Pro Tip: Check your condo downpayment requirements early. Beyond the 5% cash downpayment, Buyer’s Stamp Duty on a S$1.46M EC can exceed S$36,000 and must come from cash, not CPF.

Lifestyle and community benefits

One persistent myth is that EC living means compromising on facilities. That simply is not true. Most EC developments include full condominium facilities: swimming pools, gyms, function rooms, landscaped gardens, and 24-hour security. The physical product is comparable to a mid-range private condo in the same suburb.

What makes EC living distinctive is the community composition. Because owners cannot sell or rent out the entire unit during the Minimum Occupation Period, the resident base skews heavily toward owner-occupiers. That creates a neighborhood dynamic that many families specifically prefer, with less transient traffic and more stable, long-term neighbors.

Unit layouts in recent EC launches tend to prioritize families. Three and four-bedroom configurations are standard, with floor plans designed around practical family living rather than compact investor units.

For family-oriented buyers, the advantages of buying a condo in an EC development include:

- Larger average unit sizes compared to private condos at similar price points

- Suburban locations near reputable schools and mature amenities

- Quieter, resident-focused environments due to MOP restrictions

- Strong sense of community among similarly-profiled neighbors

Pro Tip: Cross-reference top Singapore condos by lifestyle fit before shortlisting ECs. Location and immediate surroundings matter as much as the development’s own facilities.

Ownership rules and the 2026 MOP changes

This is the section most buyers get wrong. Executive condo ownership comes with clear restrictions, and the rules tightened meaningfully in May 2026. Understanding them before you commit is not optional.

The most significant change: the MOP increased from 5 years to 10 years starting from the Temporary Occupation Permit date. For the first 10 years, you cannot sell or rent out the entire unit. This is a fundamental shift that affects liquidity planning for every buyer.

The ownership lifecycle works in three stages:

- Years 1 to 10 (MOP period): You must occupy the unit. No sale, no renting out the entire unit. You can rent out individual rooms, but the owner must continue to reside in the property.

- Years 5 to 10 (restricted resale): Resale is limited to Singapore Citizens and Permanent Residents only. This narrows the buyer pool even if you qualify to sell.

- After year 10 (full privatisation): The EC becomes a fully private condominium. You can sell to any buyer, including foreigners, with no restrictions.

Additional eligibility conditions every buyer must confirm:

- Singapore Citizenship is required for at least one applicant

- A valid family nucleus (spouse, children, parents, or siblings) must be formed

- Monthly household income must not exceed S$16,000

- Neither applicant should currently own private property locally or have disposed of private property within 30 months before application

The extended MOP is a deliberate policy choice to reduce speculation and protect the EC scheme’s purpose. For genuine owner-occupiers buying a family home, this is manageable. For anyone hoping to flip within five years, the calculus no longer works.

Investment considerations and long-term value

The executive condo investment reasons are grounded in data. Historical appreciation from 2014 to 2024 shows ECs averaging 40 to 60% capital gains over a 10-year hold, compared to 18 to 28% for private condos over the same period. The reason is structural, not accidental.

Two forces drive EC outperformance. First, you buy at a significant discount relative to private condos. Second, at the 10-year mark, the EC undergoes privatisation. That event triggers a measurable post-privatisation premium of 8 to 15% as the property transitions to full private condo status, attracting a broader buyer pool that was previously excluded by ownership restrictions.

After privatisation, ECs trade like regular private condominiums with wider buyer access, which directly supports pricing.

Here is how ECs stack up against private condos over a 10-year horizon:

| Category | Executive Condo | Private Condo |

|---|---|---|

| Typical 10-year appreciation | 40-60% | 18-28% |

| Entry price advantage | Yes (25-30% lower) | No |

| Privatisation premium | 8-15% at year 10 | Not applicable |

| Buyer pool post-MOP | Widened at year 10 | Always open |

| Speculation risk during MOP | Low | Higher |

That said, no asset class delivers uniform returns. Capital appreciation depends heavily on project location, your entry price relative to nearby comparables, and infrastructure development in the area. An EC near a planned MRT expansion, for example, will likely outperform one in a static suburban corridor. The URA Master Plan is the clearest forward-looking indicator of which locations are set for price growth.

Pro Tip: ECs provide resilience as owner-occupied assets. The longer MOP actually reduces market volatility in EC pricing because speculative flipping is structurally limited.

Financial planning and the buying process

Knowing the purchase price is only one part of your financial readiness. Buyers regularly underestimate the full cash commitment required.

Here is what you need to prepare beyond the headline price:

- 5% cash downpayment: This must come from cash, not CPF.

- Buyer’s Stamp Duty: Often exceeds S$36,000 on a mid-range EC and cannot be paid using CPF.

- Legal fees: Typically S$2,500 to S$3,500 for conveyancing.

- Furnishing and renovation reserve: Budget S$50,000 to S$80,000 minimum for a practical fit-out.

- Resale levy: If you previously bought a subsidized HDB flat, expect a levy of S$30,000 to S$55,000 depending on flat type.

On the financing side, the MSR limits your monthly mortgage to 30% of gross monthly income. While the Loan-to-Value ratio allows up to 75% borrowing, the MSR often cuts in first and reduces how much you can actually borrow. A household earning S$12,000 monthly, for example, can service a maximum of S$3,600 in monthly mortgage payments, which sets a hard ceiling on the loan quantum regardless of property value.

Stress-testing your repayment capacity at a 4.0% interest rate is now standard practice. If the repayment becomes uncomfortable at that rate, the purchase size needs to be reconsidered.

Pro Tip: Exercise your Option to Purchase only after confirming your financing in writing from your bank. Pre-approval letters give comfort, but formal letter of offer confirms your actual loan amount.

My perspective on ECs in 2026

I’ve advised a significant number of buyers through EC purchases, and my honest view is that the extended MOP is actually good news for the right buyer. The people who struggled with ECs in the past were those who treated them as short-term vehicles. They bought with an exit in mind and found the restrictions suffocating. The new 10-year MOP forces alignment between what ECs were designed to be and what buyers expect from them.

What I’ve learned is that the buyers who do best in ECs are those who buy for home first and investment second. The appreciation follows naturally from that discipline. When you’re not obsessing over short-term exit windows, you make better decisions about location, floor plan, and fit.

The risk I see most often is financial overreach. A household qualifying at the S$16,000 income ceiling does not automatically have the cash reserves to absorb BSD, furnishing, and potential interest rate increases. I’ve seen buyers pass their affordability check on paper and then feel the strain six months into ownership.

The EC scheme exists to serve the sandwich class in Singapore’s housing market. In 2026, it still does that very effectively. But it works best when buyers treat the 10-year commitment as a feature, not a constraint.

— Aman

How Aesthetic Havens can guide your EC purchase

Deciding whether an executive condominium fits your goals requires more than reading a guide. It takes a clear view of your financial position, eligibility status, preferred locations, and long-term wealth strategy.

At Aesthetic Havens, we work with buyers at every stage of that process, from first-timer eligibility checks to investment scenario modeling. Whether you want to understand how a specific EC launch compares to private alternatives or need to structure your finances before exercising an OTP, we provide the analysis and guidance to move with confidence. If you’re also curious how EC returns compare to other asset classes, our breakdown of commercial property investment benefits gives you a useful second perspective. Reach out today and let’s map out the right property move for your situation.

FAQ

Why buy an executive condo over a private condo?

ECs are priced 25 to 30% lower per square foot than comparable private condos, offer similar facilities, and have historically appreciated 40 to 60% over 10 years. For eligible buyers, the value proposition is stronger than most private alternatives at the same price point.

What is the MOP for ECs in 2026?

The Minimum Occupation Period increased to 10 years starting May 2026. You cannot sell or rent out the entire unit for the first decade from the Temporary Occupation Permit date.

Is an executive condo worth it as an investment?

Yes, for buyers with a genuine 10-year horizon. The privatisation event at year 10 typically delivers an 8 to 15% premium on top of general appreciation, and ECs have outperformed private condos historically over comparable hold periods.

Who is eligible to buy an EC in Singapore?

At least one applicant must be a Singapore Citizen, a valid family nucleus must exist, and household income must not exceed S$16,000 per month. Neither applicant should currently own private property locally.

What hidden costs should EC buyers prepare for?

Beyond the 5% cash downpayment, buyers need cash reserves for Buyer’s Stamp Duty, legal fees, furnishing, and potentially a resale levy if upgrading from a subsidized HDB flat. Total cash requirements can easily exceed S$100,000 on top of the downpayment.