Rental yield is one of those numbers every Singapore landlord thinks they understand until they actually run the math. Many investors quote a 4% or 5% figure based on raw rent and purchase price, then wonder why their cash flow tells a different story. The gap almost always comes down to expenses that never made it into the calculation. This guide cuts through that confusion by explaining exactly what rental yield means, how to calculate both gross and net versions, which costs you must include, and how to use yield data to make sharper investment decisions across Singapore’s residential and commercial property landscape.

Table of Contents

- Understanding rental yield: The foundation of property returns

- Gross vs net rental yield: Key differences and formulas

- What counts as rental expenses in Singapore?

- Using rental yield to make smarter Singapore property investments

- Our take: Why net yield is the only number that matters

- Ready to optimize your rental returns in Singapore?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Focus on net yield | Net rental yield offers a clearer picture of your real property returns than gross yield. |

| Include all expenses | Always account for ongoing costs like taxes, maintenance, and vacancies in your yield calculations. |

| Compare properties wisely | Use rental yield to evaluate and compare investment opportunities in Singapore’s property market. |

| Regularly update calculations | Review and adjust your yield as rental rates and expenses change over time. |

Understanding rental yield: The foundation of property returns

At its core, rental yield is the annual rental income from a property expressed as a percentage of its purchase price or value. That single percentage tells you how hard your money is working each year through rent alone, separate from any price appreciation the property might enjoy.

Why does this matter so much? Because Singapore property is expensive. When you commit hundreds of thousands or even millions of dollars to an asset, you need a clear, consistent way to measure what that capital is generating. Rental yield gives you that benchmark. It lets you compare a two-bedroom condo in Toa Payoh against a studio in Jurong, or a shophouse in Chinatown against an industrial unit in Ubi, using one standardized number.

It is also important to separate rental yield from capital appreciation. Both are legitimate return sources, but they behave very differently. Capital appreciation is unrealized until you sell. Rental yield, on the other hand, shows up in your bank account every month. For investors who need cash flow to service loans or fund living expenses, yield is the metric that actually keeps the lights on.

Here are the key situations where rental yield should guide your decision:

- Comparing two or more properties at different price points

- Evaluating whether a rent increase justifies the cost of renovation

- Assessing portfolio performance across multiple units

- Deciding whether to hold, sell, or refinance an existing investment

- Screening new acquisitions before committing to due diligence

You can explore typical rental yield values across different Singapore property types to set realistic benchmarks before you run your own numbers. The Singapore rental market overview also provides useful context on how rents have moved across districts and property classes.

Pro Tip: If your property has appreciated significantly since purchase, recalculate yield using the current market value, not the original price. This gives you a true picture of your opportunity cost and whether holding still makes financial sense.

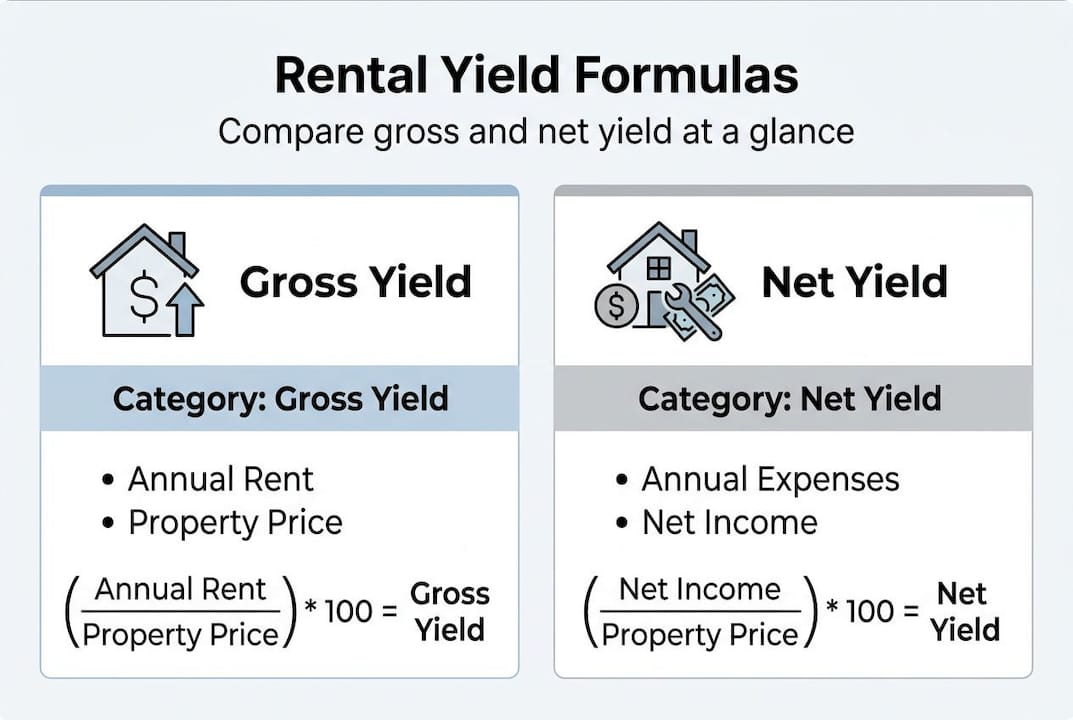

Gross vs net rental yield: Key differences and formulas

There are two main types of rental yield every investor needs to know: gross rental yield and net rental yield. Confusing them is one of the most common and costly mistakes in property investing.

Gross rental yield is the simpler of the two. The formula is straightforward:

Gross Rental Yield = (Annual Rent / Property Price) x 100

For example, if you own a condo worth SGD 1,200,000 and it rents for SGD 3,500 per month, your annual rent is SGD 42,000. Divide by SGD 1,200,000 and multiply by 100, and you get a gross yield of 3.5%. Clean and easy.

Net rental yield is what you actually earn after expenses. The formula is:

Net Rental Yield = [(Annual Rent – Annual Expenses) / Property Price] x 100

Using the same property, if your annual expenses total SGD 12,000 (taxes, maintenance, agent fees, insurance, and vacancy allowance), your net annual income drops to SGD 30,000. Divide by SGD 1,200,000 and you get a net yield of just 2.5%. That one percentage point difference represents SGD 12,000 a year in real money.

| Feature | Gross rental yield | Net rental yield |

|---|---|---|

| Formula | (Annual Rent / Price) x 100 | [(Rent – Expenses) / Price] x 100 |

| Includes expenses | No | Yes |

| Reflects cash flow | No | Yes |

| Best used for | Quick property screening | Final investment decisions |

| Accuracy | Lower | Higher |

Here are the steps to calculate calculating gross and net yield for any Singapore property:

- Confirm the annual rental income based on current or projected market rent

- Identify the property’s current market value or purchase price

- Divide annual rent by property value and multiply by 100 for gross yield

- List all annual expenses including taxes, maintenance, fees, and vacancy buffer

- Subtract total expenses from annual rent

- Divide the result by property value and multiply by 100 for net yield

Pro Tip: Net rental yield is the number that actually reflects your cash flow. Use gross yield to filter options quickly, but always finalize decisions based on net yield.

What counts as rental expenses in Singapore?

Net rental yield subtracts annual expenses like maintenance, taxes, agent fees, insurance, and vacancy from annual rent. But knowing which costs to include and how much to budget for each is where most landlords fall short.

Here are the main recurring expense categories for Singapore landlords:

- Property tax: Residential properties rented out are taxed at progressive rates starting from 12% of the annual value under the non-owner-occupied tier

- Maintenance and conservancy fees: Monthly charges for condos typically range from SGD 300 to SGD 600 depending on facilities and unit size

- Agent or management fees: Typically one month’s rent for a new tenancy, or 8% to 10% of monthly rent for full property management

- Landlord insurance: Usually SGD 200 to SGD 500 annually for a standard residential unit

- Repairs and ad hoc maintenance: Budget at least 1% of property value per year for unexpected fixes

- Vacancy allowance: Assume at least one month of vacancy per year to stay conservative

| Expense category | Estimated annual cost (SGD) |

|---|---|

| Property tax | 3,000 to 8,000 |

| Maintenance fees | 3,600 to 7,200 |

| Agent fees (annualized) | 3,000 to 4,500 |

| Landlord insurance | 200 to 500 |

| Repairs and maintenance | 5,000 to 12,000 |

| Vacancy allowance | 3,000 to 4,500 |

| Total estimate | 17,800 to 36,700 |

Hidden costs are where investors lose money quietly. Stamp duty on lease agreements, legal fees for tenancy disputes, and the cost of repainting or refurnishing between tenancies all add up. Always build in a 10% buffer on top of your estimated expenses.

Expense profiles also vary by property type. HDB flats tend to have lower maintenance fees but stricter rental rules. Condos carry higher conservancy charges but attract tenants willing to pay premium rents. Commercial and industrial units often shift more maintenance responsibility to tenants, which can improve your net yield significantly. You can find targeted property investment tips based on property type to sharpen your expense planning.

Using rental yield to make smarter Singapore property investments

Rental yield is a cornerstone metric for evaluating property returns, but its real power shows up when you use it actively rather than just calculating it once at purchase.

Here are the most effective ways to put yield data to work:

- Compare properties side by side using net yield, not asking price

- Track yield changes year over year to spot when a property is underperforming

- Use yield to justify rent increases to existing tenants with market data

- Benchmark your portfolio against rental income benchmarks for similar Singapore districts

- Identify when selling and redeploying capital into a higher-yield asset makes more sense than holding

Common investor mistakes are worth calling out directly. Many landlords focus on gross yield because it looks better on paper. Others underestimate vacancy, assuming their unit will rent immediately every time. Both habits lead to cash flow surprises that erode actual Singapore property returns.

Here is a quick real-world comparison. Property A is a two-bedroom condo in District 9 priced at SGD 1,800,000 renting for SGD 4,500 per month. Gross yield is 3.0%. After SGD 28,000 in annual expenses, net yield drops to 1.4%. Property B is a two-bedroom condo in District 19 priced at SGD 1,100,000 renting for SGD 3,200 per month. Gross yield is 3.5%. After SGD 18,000 in expenses, net yield comes in at 1.9%. Property B wins on net yield despite the lower headline rent.

“Investors who focus exclusively on gross yield often discover their actual returns are 30% to 40% lower than expected once expenses are properly accounted for.”

Pro Tip: Factor in projected rent changes and expense increases over the next three years when calculating yield. A property that yields 2.5% today but sits in a high-demand district could look very different in 24 months.

Our take: Why net yield is the only number that matters

Gross yield is a marketing number. It looks clean, it sounds impressive at dinner parties, and it is almost always misleading. We have seen experienced investors commit to properties in premium Singapore districts based on a 4% gross yield, only to discover their net yield barely clears 2% once all costs are accounted for.

The uncomfortable truth is that Singapore’s high property prices, progressive tax structure, and rising maintenance costs make expense management just as important as rent collection. A landlord who earns SGD 4,000 per month in rent but spends SGD 1,800 on costs is not a 4% yield investor. They are a 2.2% yield investor with a 4% illusion.

We encourage every landlord and investor we work with to revise their due diligence process so that net yield is the first and final filter. Not location. Not gross rent. Net yield. Explore our insights for Singapore investors for frameworks that put this into practice across different property strategies.

Comparing investment opportunities on gross yield alone is like comparing two cars on horsepower while ignoring fuel costs, insurance, and maintenance. The sticker number rarely tells the full story.

Ready to optimize your rental returns in Singapore?

Understanding rental yield is the first step. Applying it to the right properties, in the right districts, with the right expense structure is where real returns are built.

At Aesthetic Havens, we work with Singapore landlords and property investors to identify opportunities that deliver genuine net yield, not just attractive gross figures. Whether you are reviewing your existing portfolio or evaluating your next acquisition, our expert Singapore property services give you the data, analysis, and on-the-ground knowledge to make confident decisions. Reach out today and let us help you build a property portfolio that performs where it counts.

Frequently asked questions

How do I calculate rental yield for my Singapore property?

Gross rental yield is (annual rent / price) x 100; for net yield, subtract your total annual expenses from annual rent before dividing by the property price. Both calculations give you a percentage that benchmarks your income return.

What is considered a good rental yield in Singapore?

Residential properties in Singapore typically yield between 2% and 4%, with higher yields generally found in suburban districts and smaller unit types. Commercial and industrial properties can yield higher but carry different risk profiles.

What expenses should be included when calculating net rental yield?

Net rental yield subtracts annual expenses including maintenance fees, property tax, agent fees, landlord insurance, repair costs, and a vacancy buffer. Missing any of these will overstate your actual returns.

How does rental yield differ from capital appreciation?

Rental yield measures the income your property generates each year as a percentage of its value, while capital appreciation is the increase in the property’s market price over time. Both contribute to total returns but behave very differently in terms of timing and liquidity.

Why is net rental yield more important than gross rental yield?

Gross does not account for expenses; net yield does, showing your true cash flow position. In Singapore’s high-cost environment, the gap between gross and net can easily be one to two percentage points, which represents a significant difference in real money.